Accelerating Healthcare Payments with Straight Through Processing

Posted on

Key Takeaways

Healthcare reimbursement friction is rarely one big problem—it’s hundreds of micro-frictions that slow posting, drain staff time, and add risk in high-stakes environments.

Straight Through Processing (STP) is positioned as a practical “overlay” that removes manual steps without forcing workflow changes or downtime for revenue cycle teams.

STP focuses on speed + visibility: next-day funding after approval and claim-level reporting packaged with payments.

When I transitioned from Customer Experience into Payments at CSG, I expected to deepen my understanding of the financial mechanics behind healthcare, but I didn’t anticipate how much these conversations would widen my perspective. What’s become clear in my discussions with providers is that, despite everything on their plates, they’re willing to engage in conversations that can genuinely reduce friction for their teams.

Hospitals and health systems aren’t just managing patients; they’re managing reimbursements, claims data, virtual cards, the tail end of paper processes, reporting gaps, enrollment steps, and vendor ecosystems that rarely speak the same language.

When your business is literally saving lives, payment workflows shouldn’t be one more thing you need to triage.

The hidden friction in today’s reimbursement experience

Payment modernization in healthcare is rarely about solving one big problem. As with any change in a complex system, it faces a thousand micro-frictions that add up. Providers tell me about:

Managing reimbursements split between virtual cards, manual checks, and digital methods

Wrestling with fragmented reporting that slows down posting

Relying on back-office staff to manually reconcile paper or PDF remittances

Processes that break whenever patient volume spikes or staff bandwidth shrinks

None of these frictions individually feels catastrophic, but together they drain time, slow revenue cycles, and add complexity to high-stakes environments.

That’s why STP has become such an energizing topic. Not because it’s “new,” but because it’s practical, accessible, and easy for providers to adopt, especially through the combined strengths of CSG and Optum Financial.

Why this partnership matters

CSG’s platform has always been built for scale, speed, and reliability. Optum Financial brings an unmatched healthcare network reach and established reimbursement rails. Combine the two, and you get something transformational.

1. Faster, predictable funding without operational disruption

Once a claim is approved, funds are typically disbursed the next day. Providers don’t need to wait for paper, batch cycles, or multistep workflows. It’s speed without a downside.

2. Automation that removes manual work, not adds to it

Straight Through Processing isn’t about changing the way providers work; it’s about quietly removing steps that slow them down. STP “piles onto their existing tech stack” in a good way, meaning no downtime, no workflow changes, and no operational burden for revenue cycle teams who already have too much on their plates.

3. Comprehensive visibility with claim-level detail

Our reports package claims data with corresponding payments. This summarizes stacks of benefits explanations (or EOBs) with clean, structured data that’s available in just a few clicks.

4. A single payments partner for the entire healthcare ecosystem

Executives love hearing that their entire payment footprint can be unified, and, as I tell them in our conversations, “we can do everything from the gift shop to the parking lot to the cafeteria all the way back to patient payments.”

Paper checks: the last mile of reimbursement we can finally retire

Paper checks are fading, but they’re not yet gone. Interestingly, many leaders tell me they’re only receiving “one or two checks a month” now. But even a single paper check still requires staff time, introduces manual posting, and creates unnecessary operational noise. Smaller, regional practices tend to feel this pain more intensely, often relying on heavier check volumes.

Regardless of size, the opportunity is the same: digitize the last mile and eliminate unnecessary steps. STP closes that loop.

The simplicity providers are asking for

One of the most repeated themes from executives is that they don’t want “another system” or “another workflow.” They want clarity and simplicity.

The beauty of the STP approach is that simplicity is the product.

Enrollment is fast, intuitive, and requires no underwriting. It’s truly “a two-minute process,” as I describe it. Revenue cycle leaders love hearing that. And beyond enrollment, the day-to-day experience is seamless. STP works in the background so teams can stay focused on work that moves patient care forward.

Looking ahead: a future of integrated, intelligent payments

The most compelling part of being in this role right now is sitting at the intersection of provider pain points and real, solvable innovation. Every conversation, whether at a show, on a call, or during a quick debrief, helps shape the best practices we’re building.

We’re not just offering a payment rail. We’re building a reimbursement experience that is:

Automated

Transparent

Scalable

Easy to adopt

Centered on the realities of modern healthcare operations

And, most importantly, we’re doing it in a way that respects the operational pressures providers face every day. That extends directly to the providers we serve.

Let’s keep the conversation going

This blog is just one lens into the insights I’ve been gathering across dozens of executive conversations. And honestly, every discussion opens new opportunities to refine, simplify, and strengthen how payments flow across the healthcare ecosystem.

If you’re a healthcare leader navigating reimbursement modernization, I’d love to continue the dialogue. Your challenges, your feedback, and your vision for the future all help shape where we go next.

Because when payment operations are seamless, providers can focus on what matters most: delivering exceptional patient care.

Embedded Payments, Minus the Hype: An Operator’s Guide

Posted on

Key Takeaways

Embedded payments are an operating model, not just a UX upgrade: They affect underwriting, monitoring, compliance, payouts, support, and the full customer payment journey.

Early operating-model decisions matter more than the API: Teams need to decide who owns underwriting, monitoring, compliance, and customer experience before go-live.

Strong embedded payments programs align product, ops, and compliance from the start: The most successful teams define journeys, responsibilities, and metrics early, then improve performance through iterative measurement and tuning.

Forget the buzzwords and flashy demos—embedded payments aren’t just a passing trend or a quick add-on. For operators and product leaders, they represent a fundamental shift in how platforms take responsibility for every step of the payment journey.

Whether you’re eyeing new revenue streams or aiming for a seamless user experience, understanding the deeper operational implications is essential before jumping in.

This embedded payments guide is for operators and product leaders who want a non-hype view of what it really takes to plan, launch, and run embedded payments in production.

What embedded payments really means operationally

On the surface, embedded payments allow users to complete a transaction without being bounced to a separate checkout or portal. Operationally, it’s much bigger than that.

When you embed payments, your platform becomes the front door for:

Merchant onboarding and underwriting

Ongoing monitoring and risk reviews

Funding and payouts

Disputes and chargebacks

Everyday payment errors and support

Even if a partner provides the licenses and core infrastructure, banks and regulators increasingly see your platform as part of the control environment because your logo sits on the flows customers actually use.

It’s helpful to distinguish:

Embedded payments: Payment functions are built directly into your experience; onboarding, pay-ins, payouts, and reporting all live behind your login.

Integrated payments: You connect to a processor or gateway, but users may still leave your app (for example, to a hosted checkout or third-party portal).

From an operational perspective, embedded payments means you now care about:

How merchants are vetted and approved

What happens when behavior looks suspicious

How quickly and accurately funds move

What customers see when something is delayed, declined, or under review

If you’re not ready to answer those questions, you’re not ready to embed payments—no matter how clean your UI looks.

Decisions you need to make up front

Before you design a single screen, decide how you want to participate in the payments value chain. Most software platforms end up in one of three patterns.

1. Aggregator / referral-style models

You embed a provider’s onboarding and checkout, but the provider is the merchant-of-record or payment facilitator. They handle KYC/KYB, scheme rules, chargebacks, and (often) PCI scope.

Pros: Fastest time to market, lowest operational burden.

Cons: Less control over pricing and settlement, limited flexibility around edge cases, thinner economics.

2. Payment facilitation-as-a-service (PFaaS)

You look like the payment facilitator to your customers, but a specialist provider supplies the core stack: bank sponsorship, underwriting engines, settlement, and scheme-level compliance.

Pros: Better economics and UX control than pure referral, without taking on everything a registered payment facilitator does.

Cons: Shared responsibility for risk and compliance; you still have to design and run a serious program.

3. Registered payment facilitator

You become the payment facilitator. You own acquiring relationships, underwriting policies, monitoring, and settlement.

Cons: Significant time, capital, and expertise required. Expect a long runway to launch.

Across these models, you must make a few explicit calls:

Who owns underwriting and monitoring? Not just in theory—how are decisions made, audited, and adjusted over time?

How much UX and pricing control do you need? This often drives the choice between referral, PFaaS, and full payment facilitation.

How much fragmentation can you tolerate? Letting every customer bring their own processor keeps you “hands off,” but creates fragmented data, slow onboarding, and a heavy support burden when issues crop up.

Write these answers down. They are your operating model, not implementation detail.

Aligning product, ops, and compliance from the start

Embedded payments fail when product treats them as a feature, ops treats them as ticket volume, and compliance shows up late to say “no.”

Instead, map end-to-end journeys and assign clear ownership:

Product defines the target experience and promises

How fast can a typical customer go from sign-up to first payment?

What do they see when they’re “in review” or hit a limit?

How transparent are fees, payouts, and statuses?

Operations defines what happens when reality deviates

Who handles manual reviews and escalations?

How are refunds, reversals, and payout delays communicated?

What’s the playbook when a provider has an outage?

Compliance and risk define the guardrails

What data is required to approve a merchant?

What triggers enhanced due diligence or account freezes?

How do you handle sanctions hits, suspicious activity, and regulator inquiries?

A few concrete artifacts help keep everyone aligned:

A one-pager on your operating model and “who does what” (you vs. partner vs. bank)

A RACI for the full lifecycle: onboarding → processing → payouts → disputes → offboarding

Written risk thresholds (e.g., chargeback rates, unusual volume spikes) and what happens when they’re crossed

An incident and communications plan for payment failures, reviews, and delays—so customers hear from you before they start calling support

Supporting customers and end users through the change

Moving from legacy portals or redirects to embedded flows isn’t just a technical upgrade; it’s a behavior change for both your customers and their end users.

Design onboarding for speed and clarity

Onboarding is where growth and risk collide. Practical patterns include:

Progressive profiling: Start with lightweight info, then request more as customers approach go-live or hit certain thresholds.

Tiered underwriting: Auto-approve clearly low-risk merchants; route higher-risk segments or large expected volumes to enhanced review.

Clear statuses and next steps: “In review,” “approved,” “more info needed”—with specific guidance on how to move forward.

You’re balancing two clocks: your customers’ impatience to start taking payments, and your sponsor bank’s expectations around diligence. Good design shortens both.

Treat payment UX as its own product surface

Embedded payments keep users in your app—but only if you handle the details:

Use native, branded surfaces with secure components for sensitive data instead of clunky redirects.

Make errors specific and actionable: distinguish card declines, bank validation failures, and account reviews so users know what to do next.

Preserve inputs on error to avoid forcing people to start over.

Every “something went wrong” screen you eliminate reduces support tickets and increases completed transactions.

Harden account and payout changes

Account takeover and payout diversion often show up outside the payment form itself. Treat these as high-risk moments:

Require step-up authentication for payout-account changes and unusually large refunds.

Add “cool-off” periods before new payout destinations can receive funds.

Coordinate with your provider so flags in your app map to tighter controls on the payments side.

Done well, customers feel safer, not blocked.

Metrics for embedded payment success

If you can’t measure it, you can’t operate it. A solid embedded payments program tracks metrics across five dimensions.

1. Adoption and activation

Attach rate: % of eligible customers who turn on payments.

Time-to-first-payment: Days from account creation to first successful transaction.

These tell you if your value proposition is landing and your onboarding is workable.

2. Onboarding efficiency and risk discipline

Completion rate and drop-off by step.

Share of applications auto-approved vs. manual review.

Average time in review and “more info needed” loops.

Here, you’re looking for friction you can safely remove—and segments where you need stronger controls.

3. Payment performance

Authorization/success rate by payment method and flow.

Soft vs. hard decline mix and top decline reasons.

Retry performance for soft declines and network issues.

Small improvements here compound into meaningful revenue and a better end-user experience.

4. Risk and loss

Chargeback rate by segment and payment type.

Fraud loss rate and time-to-detect for suspicious patterns.

Return/NSF rates for ACH or bank debits, if you support them.

You want early warning when economics start to shift—before your provider or sponsor bank calls you.

5. Operational load and support

Support tickets per 1,000 transactions, categorized by driver (onboarding confusion, payout questions, errors, disputes).

Time to reconcile for finance teams compared to pre-embedded baselines.

Issue resolution time for payment-related incidents.

These metrics tell you whether your embedded model is actually easier to live with than the old patchwork of providers.

Embedded payments done well are a flywheel: better UX drives adoption, adoption feeds richer data, and that data helps you tune risk and performance. Done poorly, they’re just a new way to inherit complexity.

If you’re planning, rebuilding, or scaling embedded payments and want help thinking through models, responsibilities, and rollout, contact us to talk through your options.

Frequently asked questions

What are embedded payments, in plain language?

Embedded payments let users pay or get paid without leaving your platform. Instead of redirecting to a third-party checkout, you own the front-end experience for onboarding, payments, payouts, and reporting, even if a provider handles the underlying processing.

How is embedded payments different from “integrated” payments?

Integrated payments usually means “we connected to a processor or gateway.” Users may still be redirected or forced into a standalone portal. Embedded payments keep users inside your UI for the whole journey, with your platform acting as the front door to payment-critical workflows.

Do we have to become a registered payment facilitator to offer embedded payments?

No. Many platforms start with referral/aggregator or payment facilitation-as-a-service (PFaaS) models. These let you embed payments and earn revenue while your partner handles most scheme-level compliance and underwriting.

Who owns KYC/KYB and AML in embedded models?

In payment facilitation and PFaaS setups, the payment facilitator and sponsor bank usually hold the primary regulatory obligations. But your team still needs to collect accurate data, align onboarding flows to policy, and cooperate with ongoing monitoring.

What metrics should we track to know if embedded payments are working?

Strong programs track attach rate, time-to-first-payment, authorization rate, chargeback and fraud rates, and support tickets per 1,000 transactions—broken down by segment and payment method.

How Flexible Payment Options Change Customer Behavior

Posted on

Key Takeaways

Rigid payment rules drive abandonment and support volume: One-size-fits-all payment experiences create friction that leads customers to delay payment, abandon digital channels, or call for help instead.

Flexible payment options improve completion and on-time payments: Scheduled, recurring, guest, and structured partial payment options help customers stay current and use digital channels with more confidence.

Flexibility works best when paired with guardrails and measurement: Clear rules, strong disclosures, layered security, and a simple scorecard help organizations expand payment choice without increasing risk or operational chaos.

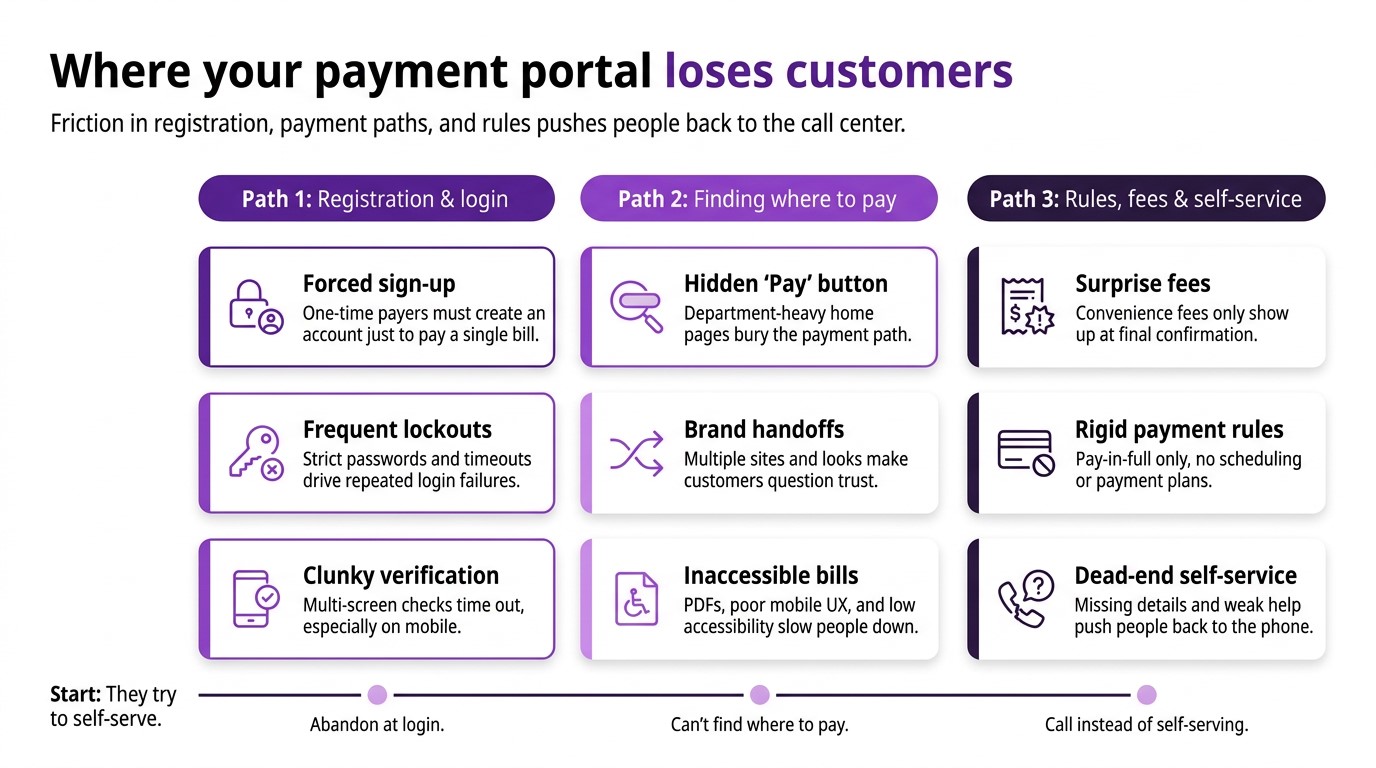

Most people only think about your payment portal as a line item on their to-do list. They want to pay their bill, avoid a late fee, keep service on, and move on with their busy, task-filled day.

That’s why when the only path to “paid” is rigid, confusing, or time-consuming, they don’t just get frustrated. They change their behavior: they abandon your portal, delay payment, and often call to ask questions instead of self-serving online.

When you introduce flexible payment options—the ability to pay as a guest, schedule or automate payments, and handle larger balances in structured ways—you give customers more than convenience. Over time, you retrain how they pay: which channels they prefer, how early they act on a balance, and how often they need staff to step in.

This piece looks at why rigidity backfires, which flexible options matter most, how they change behavior, and how to keep risk in check while you measure real impact.

Why rigidity in payments backfires

Many organizations arrive at rigid payment experiences for understandable reasons. They want to keep rules simple, manage risk, or fit legacy system constraints. But in practice, rigidity turns into friction that shows up as late payments, abandoned sessions, and higher support volume.

Common rigid patterns include:

“Pay in full now” as the only option for large or unexpected bills, with no way to pay part of the balance or spread it over time.

No ability to schedule payments around paydays, even when customers know they’ll have funds on a specific date.

Forced account creation and complex login steps for simple, one-time obligations.

Late-stage surprises, such as fees or penalty rules that only appear on the final confirmation screen.

From the customer’s perspective, these rules don’t feel “safe” or “efficient.” They feel inflexible and risky:

If they can’t pay the full amount today, they may delay payment or call to negotiate ad-hoc arrangements.

If they’re forced to register or navigate multiple redirects, they’re more likely to abandon the portal and default to phone or in-person payments instead.

If they see unclear fees or ambiguous balances at the end, they may back out entirely rather than risk paying the wrong amount.

In short, rigidity funnels “willing to pay” customers into workarounds that are slower, costlier, and harder to scale.

Examples of flexible options customers value

Flexibility doesn’t mean offering every possible configuration. It means adding a focused set of options that match how people actually manage money—across pay cycles, devices, and channels. Internal customer research and portal data highlight a few options that consistently change outcomes.

1. Guest pay with a clean, fast path

Customers want to go from “I got a bill” to “payment confirmed” in as few steps as possible, especially on mobile. Allowing one-time guest payments—without forced registration—removes a major barrier for simple obligations. When “Pay now” is easy to find, fields are minimal, and confirmation is immediate, more people complete the payment right away instead of deferring it.

2. Scheduled and recurring payments

Scheduled one-time payments and recurring/autopay let customers align payments with their cash flow and forget about due dates. For ongoing obligations—rent, utilities, premiums, tuition—these options turn a monthly decision into a background process, as long as controls and confirmations are clear.

3. Structured partial and installment payments

For larger or long-term balances, structured partial payments and installment plans can be the difference between “can’t pay” and “can get back on track.” Examples include:

Letting customers pay a defined portion of the balance now and schedule the rest.

Offering fixed-term installment plans with transparent terms and consequences.

These options give customers a realistic path to stay current without relying on one-off exceptions.

4. Multiple payment methods in one place

Customers increasingly expect to choose their rail—card, ACH/eCheck, or digital wallet—within the same experience. Supporting these options in a single, branded portal reduces channel-switching and helps people pay in the way that feels fastest and most familiar.

5. True self-service controls around payments

Flexibility also means letting customers manage how they pay over time: updating stored methods, changing contact preferences, pausing or adjusting autopay, and resolving basic “where is my payment?” questions without calling. When these capabilities are in place, customers experience the portal as a tool they control—not a locked-down system they have to work around.

4 behavior changes organizations see after adding flexibility

When organizations simplify flows and introduce targeted flexible payment options, they see more than a short-term bump in digital usage. Over time, customer behavior shifts in measurable ways.

1. Higher digital completion rates (and fewer channel switchers)

Removing hurdles like forced registration and rigid “pay in full” requirements makes it easier for customers to finish what they started in the portal. Rather than abandoning a session to call, more payers complete the transaction online, which improves digital adoption and reduces pressure on phone and in-person channels.

2. More on-time payments and fewer chronic delinquencies

When customers can schedule, split, or automate payments, they’re more likely to pay on time, avoid service disruptions, and stay current without repeated outreach or manual arrangements. Structured flexibility replaces ad-hoc exceptions with predictable, trackable behavior.

3. Fewer exception calls and manual workarounds

As options like payment plans, recurring payments, and self-service updates become standard, staff spend less time negotiating one-off accommodations or manually fixing preventable issues. Internal data shows that pairing flexible options with digital reminders and self-service tools can meaningfully reduce late payments and manual collection work.

4. Greater trust in the digital channel

Clear billing, upfront rules, and strong confirmations build trust that “my action counted.” Over time, that trust changes customer defaults: instead of thinking “I should call to be sure,” they return to digital first because it feels reliable and transparent.

Guardrails to keep risk and abuse in check

Flexibility without structure can introduce new risks: overextended customers, inconsistent policy enforcement, or higher exposure to fraud and disputes. The goal is not “flexibility at any cost,” but flexibility with clear guardrails—backed by systems that enforce them.

Key guardrails include:

Defined eligibility rules: Decide which customers, balances, and products qualify for partial payments or plans (for example, based on balance size, tenure, or past behavior) and enforce those rules through configuration, not case-by-case decisions.

Standardized plan templates: Offer a small number of well-tested plan designs (such as fixed-term installments) with clear terms, minimum payments, and consequences for missed installments, instead of bespoke arrangements each time.

Transparent, early disclosures: Surface fees, penalties, partial-payment limits, and plan rules before the final confirmation step, so customers can choose the option that fits without feeling surprised or misled.

Layered security and risk monitoring: Combine secure logins, protected account changes, and intelligent, cross-channel fraud monitoring so that expanded options (like stored payment methods or recurring debits) don’t open the door to account takeover, card testing, or ACH abuse.

Consistent policies across channels: Align rules for partial payments, plans, and fees across web, mobile, IVR, text-to-pay, and agent-assisted flows so customers don’t get different answers depending on where they happen to pay.

With these guardrails in place, you can give customers more ways to pay without sacrificing compliance, cash flow, or security.

Measuring impact on on-time payments and satisfaction

To prove that flexible payment options are changing behavior—and not just adding features—it’s important to treat flexibility as a measurable product change, not a one-time project. The same “before and after” mindset you’d use for any customer experience improvement applies here.

Start with a baseline, then track:

Completion rates and drop-off points

Measure how many customers start and finish a payment, and where they abandon, especially on mobile. Watch what happens to these numbers after you launch guest pay, scheduled payments, or plans.

Digital vs. offline payment mix

Track shifts from phone and in-person payments to web, mobile, text-to-pay, and IVR as you roll out new options.

On-time payment and delinquency rates

Compare on-time rates—and aging buckets if applicable—before and after adding structured partial payments, recurring options, or reminder flows tied to those options.

Billing- and payment-related call volume

Monitor calls tied to bill confusion, payment status, and “can I set up a plan?” requests. Effective flexibility and self-service should gradually lower these volumes as customers handle more on their own.

Qualitative feedback

Review comments from surveys, support interactions, and usability sessions for language about clarity, control, and trust. Look for a shift from “I can’t do X” and “I don’t understand Y” to “It was easy to…”.

Combining these metrics into a simple scorecard—revisited quarterly—helps you see where flexibility is working, where friction lingers, and where to invest next.

Make flexible payments easier for customers and your team

Rigid payment experiences create more work for everyone: more abandoned sessions, more exceptions, more late payments, and more calls. By introducing a focused set of flexible payment options—guest pay, scheduled and recurring payments, structured partial and installment plans—backed by clear communication, self-service tools, and strong guardrails, you can change how customers behave in lasting ways.

CSG helps organizations modernize digital bill payment experiences with:

Hosted bill payment portals that support guest and registered users, one-time, scheduled, and recurring payments, and omnichannel options like web, mobile, and text-to-pay.

Integrated acceptance for cards, ACH, eChecks, and digital wallets on a single platform, with centralized reporting and controls.

Growth and retention tools like Account Updater, ACH validation, and recovery solutions that keep recurring payments flowing and reduce declines, returns, and manual collections.

If you’re ready to see how flexible payment options could change your customers’ behavior—and your team’s workload—contact us to talk through the right approach for your organization.

Frequently asked questions

What are flexible payment options?

Flexible payment options let customers pay in the way that best fits their situation—for example, one-time, scheduled, or recurring payments; card, ACH, or digital wallets; and partial or installment payments for larger balances, all within defined rules.

How do flexible payment options change customer behavior?

When customers can schedule, split, or automate payments, they are more likely to pay on time, avoid service disruptions, and stay current without calling to negotiate exceptions, which also reduces operational strain on billing and support teams.

Which flexible payment options do customers value most?

Consistently high-value options include guest pay for one-time bills, scheduled and recurring payments, the ability to pay by card or ACH in one portal, and structured partial or installment plans for larger balances.

How can we keep flexible payments secure and compliant?

Pair flexibility with layered security: secure logins, protected account changes, tokenized payment data, and intelligent risk monitoring across channels, so you can spot suspicious patterns without blocking good users.

Where can I learn more about reducing friction and adding flexibility?

From Click to Cash: Payments Experiences ISVs Can Use to Improve Conversion

Posted on

Key Takeaways

The payments experience deserves its own design focus: Even small breaks in the flow—extra steps, confusing errors, redirects—directly reduce conversion and increase churn.

High-converting payment experiences combine seamless UX with smart controls: The strongest ISV flows use embedded payments, bill payment patterns, and growth-and-retention tactics like progressive onboarding, context-aware friction, and clear, branded error states.

Payments should be managed like a measurable product journey: Guide every step, track drop-off by segment and device, and iterate with your embedded payments partner to improve authorization, activation, and upgrade rates over time.

For independent software vendors (ISVs), your payments experience is no longer “just” plumbing. It’s one of the most important product journeys you own—and a direct driver of trial-to-paid conversion, upgrade adoption, and long-term retention.

Your customers expect to onboard, accept, and reconcile payments without ever leaving your platform. At the same time, they’re comparing you to the best digital experiences they use every day. If your flows feel clunky, confusing, or risky, they abandon—and they remember.

The opportunity for ISVs is clear: design a payments experience that turns intent into revenue—while your embedded payments partner helps you manage the complexity of risk, compliance, and scale.

This article walks through how to do that, from core customer experience principles to mobile design and analytics.

In this post, you’ll discover actionable strategies for building a seamless payments experience that boosts conversion and reduces customer churn.

Why payments deserves its own design focus

The payments experience is different from the rest of your product for three reasons:

It happens at peak intent: By the time someone lands on your checkout, upgrade, or “pay now” screen, they’ve already said “yes” in their mind. Any friction you introduce here has an outsized impact on revenue.

It sits at the intersection of money, trust, and compliance: Payment flows must satisfy end users, your merchants, card networks, banks, and regulators—all at once. Even if you use an embedded payments partner, how you collect data affects what’s possible for KYC/KYB, AML, Nacha, PCI, and ongoing monitoring.

It’s a shared journey across multiple models: The same user might pay an initial invoice, set up recurring billing, update a card, switch to ACH, or make an in-app one-time upgrade. Treating each of those flows as separate one-offs leads to inconsistent experiences and fragmented data.

Key elements of a high-converting payment flow

A high-converting payments experience does two things well:

Removes unnecessary friction at the moment of payment

Applies the right amount of smart friction when risk actually increases

Several design patterns show up consistently in ISVs that convert well.

1. Progressive profiling and tiered underwriting

Onboarding is where growth and risk collide. Ask for everything up front and users stall. Ask for too little and your risk team gets nervous.

A better pattern is:

Progressive profiling: Start with lightweight data (business name, email, basic use case) and request more only as the customer approaches go-live, higher volume, or riskier features (e.g., higher-ticket transactions, payouts).

Tiered underwriting: Auto-approve low-risk merchants; route higher-risk verticals and large volumes to enhanced review with clear expectations.

This approach reduces form fatigue, gets more customers to first payment quickly, and still gives your embedded payments or payment facilitation-as-a-service (PFaaS) partner what they need for KYC/KYB and risk decisions.

2. Native, branded payment surfaces with secure components

Redirection is the enemy of trust. When users are bounced to a third-party checkout with different branding, drop-off tends to rise.

Instead:

Keep users inside your product’s UI using embedded or hosted components for card and bank data.

Offload sensitive fields to your payments partner’s secure, PCI-compliant elements, while you control layout, copy, and brand.

This is where embedded payments shine: you get a consistent, in-product feel with a partner handling encryption, tokenization, and compliance behind the scenes.

3. Clear, actionable error states

Payment failures will happen. How you surface them determines whether users recover—or give up.

Design for:

Specific messages: Distinguish “card declined,” “insufficient funds,” “account under review,” and “suspected fraud” instead of vague “Something went wrong” errors.

Inline guidance: Show users exactly which field needs attention and what to do next.

No data loss: Preserve form inputs when an error occurs so people don’t have to start over.

This not only improves conversion; it also reduces inbound tickets and time-to-resolution for your support team.

Reducing friction at checkout and in-app upgrades

Many ISVs lose revenue in two high-value places:

The first-time checkout (initial subscription, license, or setup fee)

In-app upgrades (add-ons, more seats, higher usage tiers, new modules)

These flows are often owned by different teams, use different patterns, and may not even share analytics. The user, however, just experiences paying your company.

To reduce abandonment:

1. Make the path to pay obvious and fast

For first-time checkout, minimize clicks from “start trial” or “subscribe” to “payment confirmed.”

For in-app upgrades, trigger the payment step directly from the feature or limit the user just hit—no detours through generic account pages if you can avoid it.

Short, linear paths with clear progress indicators tend to outperform complex, multi-step wizards.

2. Offer the right mix of methods, not every method

Too many options can be as paralyzing as too few.

At minimum, support major cards and at least one lower-cost method like ACH where it fits your use case—especially for recurring bill payments and higher-ticket B2B invoices.

Prioritize the methods your segments actually use. For example, small businesses might lean more on cards, while enterprise customers prefer invoice plus ACH.

Tie this into your bill payments strategy so that whether someone is paying an invoice, auto-paying a subscription, or upgrading an account, they see familiar, trusted options.

3. Make upgrades feel reversible and safe

Users hesitate to upgrade when they’re unsure what will happen if something goes wrong.

Your upgrade flows should clearly answer:

When will I be charged?

How will this appear on my bill or invoice?

Can I roll back if it doesn’t meet my needs?

Simple answers reduce last-minute abandonment and encourage experimentation with higher tiers.

Designing payment experiences for mobile users

Mobile is often the first place users hit your limits: logging in from the field, paying a bill on the go, or approving a last-minute upgrade.

Designing a great mobile payments experience ISVs can rely on means taking small screens—and sometimes spotty networks—seriously.

1. Optimize forms for thumbs, not mice

Use single-column layouts with large tap targets.

Trigger numeric or email keyboards automatically for relevant fields.

Support autofill for address, name, and card data where possible.

The less typing required on a phone, the better your chances of completion.

2. Embrace express and wallet options

Digital wallets like Apple Pay and Google Pay can be powerful for mobile: they compress multiple steps (card entry, billing address) into a single action that feels safe and familiar.

Consider:

Offering wallets alongside cards and ACH where your risk and business model allow.

Prioritizing wallets for one-time or low-amount transactions, while steering recurring or higher-value payments toward methods that support your margin and cash-flow goals.

3. Design for low connectivity and interruption

Mobile payers get interrupted. Make sure:

Sessions can recover gracefully if a user temporarily loses connectivity.

Key states (e.g., “Payment submitted, processing…”) are clearly communicated to prevent duplicate attempts.

Users can quickly confirm status in their account or billing history without calling support.

If you’re ready to design a payments experience that actually improves conversion—and want a partner who understands both UX and compliance—contact us to talk through your roadmap and see what’s possible for your platform.

Frequently asked questions

What is a payments experience for ISVs?

It’s the end-to-end journey your customers and their end users go through to sign up, pay, get paid, and manage billing inside your software—from onboarding and KYC/KYB to checkout, refunds, recurring billing, and reporting. For many ISVs, this includes embedded payments, bill payment flows, and growth-and-retention tools like account updater or recovery workflows.

Why does payment UX matter so much for conversion?

Because payments sit at the highest-intent moment in your funnel. Every extra field, redirect, or unclear error is a place users can abandon. ISVs that streamline these steps typically see higher trial-to-paid conversion, more successful upgrades, and better retention, without changing their pricing or acquisition strategy.

Do we need to become a full payment facilitator to improve our payments experience?

Not necessarily. Many ISVs start with an embedded payments partner using models like PFaaS or referral/aggregator arrangements. These approaches let you embed modern UX patterns while your partner handles most of the underlying acquiring, risk, and compliance. You can always move toward more ownership later as volume and capabilities grow.

How does this apply if our revenue is mostly bill payments, not classic e-commerce?

The same UX principles apply. Whether you’re powering rent collection, invoices, membership dues, or usage-based billing, you still need clear amounts, flexible options, mobile-friendly flows, and predictable error handling. A unified approach across bill payments and card-present/card-not-present commerce makes it easier to measure and improve overall payment performance.

Where can we learn more about embedded payments models for ISVs and fintechs?

CSG Forte offers an overview of embedded payments and operating models like aggregators, PFaaS, and Registered Payment Facilitation in this blog: Embedded Payments for Fintechs: Scale, Compliance, & Control.

How Embedded Payments Help Insurance Agencies Simplify Billing and Grow Revenue

Posted on

Key Takeaways

Embedded payments bring premium collection into insurance workflows: Agencies, MGAs, and platforms can collect premiums, fees, refunds, and related payments inside the systems they already use instead of sending customers to disconnected third-party portals.

A unified payments layer reduces admin burden and improves retention: One platform for omnichannel payments, reporting, and reconciliation can cut manual work, improve on-time collections, and create a more consistent policyholder experience.

PFaaS gives insurance platforms a path to monetize payments without owning all the complexity: Platforms can keep control over the user experience and merchant relationships while offloading scheme-level compliance, risk, and infrastructure to a specialist partner.

Insurance billing issues create one of the most frequent—and emotionally charged—interactions policyholders have with your brand. When it’s easy to understand an insurance bill and pay it in a few clicks, your teams see faster collections, fewer calls, and better retention. When it isn’t, the opposite happens: policyholders delay or miss payments, staff chase exceptions, and churn quietly rises.

Many agencies, MGAs, and insurance platforms still rely on a patchwork of portals, processors, and homegrown tools to collect premiums and remittances. That fragmentation is exactly what embedded payments for insurance is designed to fix.

Embedded payments bring premium collection, refunds, and related flows into the systems your teams and customers already use—your agency management system, carrier portal, or insurance platform—so payments feel like a natural step in the journey instead of a detour.

This article breaks down what embedded payments look like in an insurance context, the benefits for agencies, platforms, and policyholders, and how to evaluate potential partners, including PFaaS options.

What embedded payments mean for insurance providers

At a high level, embedded payments bake payment capabilities directly into your core experiences. This means they’re a seamless, branded part of your website, not bolted on as separate sites or workflows.

In insurance, that typically includes:

Embedded checkout in policyholder portals: Policyholders can view a bill, select a payment method, and complete payment without leaving your portal or AMS.

Integrated agency and MGA workflows: Producers and staff can take payments, set up recurring premiums, or collect fees directly inside the systems where they already manage policies.

Consistent omnichannel options: Web, mobile, IVR, text-to-pay, and in-person payments all run over a common payments layer, with consistent balances and confirmation messages across channels.

Crucially, embedded payments don’t require ripping out core policy admin or billing systems. The payments layer connects to those systems via application programming interfaces (APIs) or file-based integrations, handling:

Tokenization, encryption, and storage of payment credentials

Reporting, reconciliation, and downstream file delivery

The result is a single payments fabric running through portals, agency tools, and partner platforms—rather than a maze of one-off integrations and standalone gateways.

Benefits for agencies, platforms, and policyholders

For agencies and MGAs: less manual work, more control

Agencies often sit at the intersection of multiple billing experiences: carrier portals, in-house tools, and third-party payment links that don’t talk to each other cleanly. That creates a steady stream of manual tasks:

Downloading reports from multiple portals

Reconciling premiums, refunds, and commissions by hand

Chasing down exceptions when a payment in one system doesn’t match another

Embedded payments simplify that by:

Centralizing acceptance and remittance under one platform, even when policies span multiple carriers

Standardizing files and reports, so finance and accounting teams get one set of reconciled outputs rather than many scattered ones

Enabling recurring, scheduled, partial, and over-payments from a single configuration layer, which reduces exceptions and “special cases”

With a unified embedded layer, agencies can also brand the payment experience, maintain better visibility into cash flow, and offer more consistent experiences across lines of business.

For insurance platforms: higher stickiness and new revenue

If you build or operate insurance software—AMS solutions, insurance SaaS platforms, or vertical marketplaces—embedded payments can be a powerful growth lever.

Key advantages include:

Higher adoption and retention: When agencies and carriers can handle quoting, binding, and billing in one platform, they’re more likely to standardize on your system.

Improved economics: Through payment facilitation or PFaaS models, platforms can earn a share of payment revenue instead of sending it all to third-party gateways.

Product differentiation: A cohesive, branded checkout experience that supports cards, ACH, and wallets—and offers features like reminders, autopay, and flexible plans—makes your platform harder to replace.

PFaaS is especially attractive to platforms that want payment upside without building full payment facilitator infrastructure. The PFaaS provider handles scheme-level compliance, risk, and settlement while the platform controls UX, pricing strategy, and merchant relationships.

For policyholders: simpler, more flexible ways to stay covered

Embedded payments sit at the intersection of UX, operations, and risk. A good design addresses all three.

Integration: meet your stack where it is

Most insurers and platforms can’t flip a switch and replace core policy and billing systems. Instead, embedded payments should integrate with what you already have.

Look for:

Flexible integration patterns: Modern REST APIs for real-time updates plus file-based options for systems that still rely on batch.

Unified payment layer across premiums, claim disbursements, and agency remittances: So you don’t need separate workflows for each.

Cloud-based reporting and reconciliation: That drops cleanly into finance and policy systems.

A phased approach—starting with the highest-volume premium flows, then extending to agencies, MGAs, and additional channels—limits disruption while still delivering quick wins.

Compliance and security: reduce exposure without slowing down

Insurance payments touch regulated domains: card networks, ACH rails, privacy rules, and sometimes healthcare-adjacent data. Embedded payments should shrink your risk surface, not expand it.

Non-negotiables include:

PCI DSS Level 1 infrastructure with hosted, PCI-compliant forms: So card data never touches your servers directly.

Tokenization and encryption for stored payment profiles: Enabling features like autopay and one-click renewals without storing raw card numbers.

Alignment with Nacha rules for ACH: Including account validation and appropriate handling of returns.

Clear shared-responsibility models: That spell out who owns what across fraud monitoring, disputes, and incident response.

If you serve adjacent regulated spaces (for example, health benefits or supplemental products), it’s helpful when your payments provider already treats HIPAA as a security benchmark, even if your particular use case isn’t directly in scope.

7 questions to evaluate potential embedded payment partners

When you’re comparing providers—whether for a carrier, agency group, or platform—go beyond feature checklists. Use these questions to focus on long-term fit.

1. Can they support true omnichannel insurance payments?

Ask which channels (web, mobile, IVR, text-to-pay, in-person, agent-assisted) run on the same platform, with unified balances and reporting.

2. Do they handle card, ACH, and wallets in one place?

Verify that you can offer cards, ACH/eCheck, and major digital wallets under a single contract and technology stack—and that you can shape behavior (for example, steering large annual premiums to ACH).

3. How strong is their security and compliance posture?

Look for evidence of PCI DSS Level 1 certification, tokenization and encryption, Nacha alignment, and a documented shared-responsibility model.

4. How do they integrate with policy, claims, and agency systems?

You’ll want both real-time APIs and file-based options, plus experience integrating with insurance cores, billing systems, and agency platforms similar to yours.

5. What does reporting and reconciliation look like?

Ask to see reporting dashboards and reconciliation outputs. Finance leaders should be able to get near real-time visibility across channels and entities without stitching multiple exports together.

6. Is there a path to PFaaS or payment facilitation?

For platforms and larger groups, explore whether the partner can support PFaaS or payment facilitation models when you’re ready. That way, you can start with a simple referral-style setup and graduate to monetizing payments more directly, without changing your payments stack.

7. Can they help you measure impact?

Make sure you can track on-time premium rates, failure and recovery rates, digital adoption by channel, billing-related call volume, and lapse/cancellation tied to payments—all key metrics for modernization and retention.

Where to go next

If you’re ready to move beyond a patchwork of portals and payment vendors, a unified, embedded payments layer is a practical next step.

What does “embedded payments for insurance” actually mean?

Embedded payments for insurance means premium collection, fees, refunds, and remittances happen inside your existing insurance or agency software—policy portals, agency management systems (AMS), or billing platforms—instead of redirecting customers to standalone payment sites.

How do embedded payments reduce manual work for agencies and MGAs?

With the right platform, agencies can centralize premium collection and remittances, standardize files, and feed status and settlement data straight into policy and finance systems. That reduces file downloads, re-keying, and exception handling that typically consume billing teams’ time.

What’s the difference between embedded payments and PFaaS (Payment Facilitation-as-a-Service)?

Embedded payments describe where and how payments happen—in your own workflows and UX. PFaaS is a commercial and operating model that lets an insurance platform monetize payments like a payment facilitator, while a specialist partner handles core acquiring infrastructure, onboarding, and scheme-level compliance.

Which payment methods should embedded insurance payments support?

For most insurers and agencies, the baseline is cards + ACH/eCheck, plus leading digital wallets. Cards are familiar and fast; ACH often offers lower cost and fewer lifecycle failures for large or recurring premiums. Digital wallets help mobile-centric policyholders complete payments faster.

Where can I learn more about modernizing insurance payments?

Unlock Seamless B2B Payments: How ACH Powers Modern Growth

Posted on

Every thriving business relationship relies on trust, efficiency and the seamless movement of money. Yet for too long, business-to-business (B2B) payments have been weighed down by outdated processes, endless paperwork and frustrating delays. But with the continued adoption and expansion of Automated Clearing House (ACH) payments, companies are finding new momentum—unlocking smoother transactions, reducing costs and powering growth without the usual financial friction.

Explore the value of this payment type for transactions between businesses.

What Are Business-to-Business ACH Payments?

Business to business ACH payments are electronic fund transfers between two companies. ACH payments provide a modern and secure method for processing fund transfers electronically. These transfers occur in the ACH Network and eliminate the need for paper trails that come with checks, money orders and other conventional payment methods.

ACH is a widely used electronic payment system in the United States and internationally. With this network so widely recognized, it can be an ideal solution for business to business payments between companies that are located in different states or countries.

Business to business transactions encompass a wide range of corporate processes, from paying advertisers and shipping companies to covering rent for office spaces. While many individuals have stopped using checks for their day-to-day payments, many businesses are still relying on these slips of paper to make large payments to other businesses. With corporate ACH payments, businesses can streamline a significant aspect of operations.

How Does B2B ACH Work?

All ACH payments start with two bank accounts—the Originating Depository Financial Institute (ODFI) and the Receiving Depository Financial Institute (RDFI). Essentially, there’s a bank account requesting a payment, the RDFI, and an account sending money to respond to the request, the ODFI.

In B2B ACH payments, this arrangement stays the same. However, rather than a corporate bank account and a consumer bank account, the transaction happens between two corporate accounts. The Clearing House or the Federal Reserve oversees the transaction by storing and processing the funds. Since these transactions are not direct from bank to bank, they can take one to two days to process.

The entire ACH process can be divided into four steps:

Authorization: Before funds can move from one account to another, the ODFI needs authorization from the owner of the account to transfer funds through ACH. During authorization, the business will have to provide the account and routing numbers for the corporate account and other details to verify the use of their funds. As a business requesting this authorization, you may send an email with a link to the accounting department, so they can complete the authorization process.

Initiation: The business then sends its information to the ACH provider or ODFI to initiate the transaction.

Request: After initiating the transaction, the ODFI can send a payment request to the RDFI to receive the necessary funds for a product or service.

Processing: As long as all information is correct and the RDFI account has enough funds to complete the request, processing can begin. The funds move from the RDFI account to the ODFI, and the business receiving funds will officially be paid for their product or service.

Benefits of B2B ACH Payments

Using ACH payments for your B2B transactions has many advantages, including:

Simplicity: ACH payments are easy to set up with the right ACH provider. Both companies involved only need to provide account information for their corporate bank accounts and work with a provider who supports the process. Most banks allow the ACH process to occur with authorization, so there’s no need to have a special account or change the way you manage financials for your business.

Speed: While there is a processing window for ACH payments, it is typically only a few days maximum. Even with this processing time, businesses will receive confirmation that funds are entering their account before they officially arrive. This aspect makes business to business ACH debit much easier than checks. Accounting teams don’t need to reconcile the bank account with several outstanding checks that have not yet been cashed.

Security: With many businesses still relying on checks for B2B payments, check fraud is a possibility. Businesses are particularly at risk because they send multiple checks with large amounts. ACH payments are completely electronic and verified through your ACH platform, so you know you’re genuinely receiving money from your client businesses, and information like account and routing numbers is kept private.

No processing fees: ACH payments are free of all processing fees, which is a major benefit to businesses that transfer money frequently between suppliers, clients and beyond. With so many transactions, small fees can add up and lead to large costs at the end of a month.

Low transaction fees: Transaction fees for ACH payments are often free or low in cost, depending on the financial institutions involved. Compared to wire transfers or credit card processing, these fees are incredibly cost-effective.

Electronic records: ACH payments have a clear electronic record you can access at any time, so it’s easy to manage invoicing processes, and you can cut down on paper records.

Implement ACH Processing With CSG Forte

CSG Forte’s Dex payments platform is the key to implementing ACH processing for your B2B transactions. Manage online, in-person and over the phone payments with a unified, cloud-based solution. With transparent reporting, you can stay connected to every transaction and manage your funds more efficiently.

B2B ACH payments are electronic bank-to-bank transfers made between businesses through the Automated Clearing House network. They help companies replace paper checks with a faster, more secure, and more efficient way to send and receive payments.

2. How do ACH payments work for business-to-business transactions?

ACH payments for business-to-business transactions work by moving funds electronically from one business bank account to another through the ACH network. After authorization is provided, the payment is initiated, processed by financial institutions, and deposited into the receiving business’s account.

3. How long do B2B ACH payments take to process?

Most B2B ACH payments take one to two business days to process, though timing can vary depending on the financial institutions involved and when the transaction is submitted. Many businesses value ACH because it offers predictable processing and clear electronic payment records.

4. What are the benefits of using ACH for B2B payments?

The main benefits of using ACH for B2B payments include lower transaction costs, improved security, easier payment tracking, reduced paperwork, and more efficient cash flow management. ACH can also help businesses streamline accounts receivable and accounts payable processes.

5. Are B2B ACH payments more secure than checks?

Yes, B2B ACH payments are generally more secure than paper checks because they are processed electronically through established banking networks. This reduces the risk of lost checks, mail fraud, and manual errors while giving businesses a more reliable digital record of each transaction.

G2 Spring 2026 Payment Gateway: CSG Forte Recognized by Real Customers

Posted on

CSG Forte is pleased to announce we’ve been recognized in G2’s Spring 2026 Payment Gateway Grid, which highlights providers that consistently deliver on expectations, based on customer reviews and market presence.

This recognition matters because it’s driven by the people who know our platform best—our customers and partners. Your real-world feedback powers CSG Forte’s presence on the G2 grid and helps other organizations choose a trusted payment gateway with confidence.

Who is G2—and why this recognition matters

G2 is a leading B2B software review platform where verified users rate and review the tools they use every day. Its independent reviews, category grids, and badges are widely used by software buyers to compare products based on real experiences—not just vendor claims.

For payment gateways, independent validation is especially important. Buyers want to know:

Is the platform reliable and available when payers are trying to check out?

Does it integrate smoothly with billing, CRM, and other core systems?

Can it support multiple payment methods and channels without adding operational complexity?

Is the provider focused on security, compliance, and ongoing innovation?

Where to see CSG Forte on the G2 Spring 2026 Payment Gateway Grid

The G2 Spring 2026 Payment Gateway recognition is powered by reviews from merchants, government agencies, and partners who use CSG Forte to run their day-to-day payments. In those reviews, customers frequently highlight:

Reliable payment processing that supports high volumes without adding unnecessary complexity

Strong integrations with customer relationship management, billing, and back-office systems, so payments fit cleanly into existing workflows

Flexible payment options that help organizations accept payments online, over the phone, and in person, supporting cards, ACH, and digital wallets

A focus on innovation and scalability, so their payment stack can evolve alongside new channels, regulations, and customer expectations

Hands-on support and collaboration, not just software—especially during onboarding, migrations, and peak seasons

That combination of technology, integration, and partnership is exactly what we aim to deliver with the CSG Forte payments gateway.

Have a few minutes? Share your experience with CSG Forte on G2

If you’re an existing CSG Forte merchant or partner, your feedback has already helped us earn this G2 Spring 2026 Payment Gateway recognition. If you’re open to it, we’d be grateful if you’d also share your experience directly on G2.

A few quick details:

Timing: Reviews typically take about 5–10 minutes to complete.

Privacy: Reviews can be submitted anonymously (your name and company don’t have to appear publicly).

Thank you from G2: As a thank you, the first 20 reviewers are eligible for a $25 gift card from G2 (subject to G2’s terms).

Whether you’re processing payments for a city or county, a small business, or a fast-growing software platform, your candid review helps:

Other buyers evaluate payment gateway options more confidently.

Our product and customer teams understand what’s working well and where to focus next.

CSG Forte continue to invest in the features, tools and support that matter most to you.

Thank you for helping us earn the G2 Payment Gateway badge

We’re proud to be recognized in the G2 Spring 2026 Payment Gateway Grid—and even more grateful for the customers and partners who made it possible by sharing their experiences.

If you’d like to learn more about CSG Forte’s payment gateway, explore additional resources at Forte.net, or reach out to one of our payments experts today to talk about what’s next for your payment strategy.

A Practical Model for Digital Payment Risk Management

Posted on

Key Takeaways

Online payments are now a primary fraud battleground: As more bill pay and customer transactions move online, attackers are targeting these flows with sophisticated scams, making fraud protection a front-line business priority, not a back-office concern.

AI has raised the stakes on both sides: Fraudsters now use AI to automate attacks (ATO, synthetic identities, phishing), so businesses need AI-driven tools to keep up.

Modern fraud protection must be adaptive and transparent: The strongest defenses deploy quickly, learn from your unique transaction patterns, and give you clear visibility and controls so you can cut fraud and false positives without slowing good customers down.

Digital payments are a growth engine, but only when you can keep good customers moving and bad actors out. That’s the real job of payment risk management: reducing fraud losses and reducing unnecessary friction (false declines, delayed approvals, and customer support fallout). Traditional tools often fall short because they’re slow, siloed, hard to tune, and can create as many customer experience issues as they prevent.

Why payments need a clear risk model

A clear risk model matters because payment risk isn’t one problem—it’s a chain reaction:

Fraud losses hit margin directly (plus chargebacks/returns, fees, and write-offs).

False positives hit revenue indirectly (blocked transactions, abandoned checkouts, churn, and a spike in “why was my payment declined?” support tickets).

Compliance expectations keep rising, especially in ACH fraud monitoring and card-network dispute/fraud programs.

A practical risk model gives you three things most teams don’t have today:

A shared definition of “acceptable risk” (so teams stop fighting over one-off decisions).

A map of where risk enters your payment flows (so you can fix root causes, not symptoms).

Repeatable operating rhythms (so improvements don’t disappear after the next incident).

If you want a familiar structure to align security and fraud teams, the National Institute of Standards and Technology recommends lifecycle framing—Identify, Protect, Detect, Respond, Recover—as a useful backbone to adapt to payments.

Mapping your main payment and fraud risks

Start by mapping risks across the full payment lifecycle (not just the authorization moment). A simple way to do it is to build a one-page “risk register” by journey stage:

1. Account & login (before a payment happens)

Common risks: Account takeover (ATO) via phishing, credential stuffing, or social engineering and refund redirection (fraudster changes payout details, then triggers refunds/credits).

2. Payment setup (adding or updating payment methods)

Common risks: Bad payment data and mismatched account ownership (drives downstream declines/returns and customer friction).

Common risks: Card testing (small, high-velocity attempts to find valid cards), customer payment fraud, excessive payment / refund abuse.

4. Merchant/portfolio risk (especially for ISVs, aggregators, multi-location orgs)

Common risks: Merchant bust-out fraud and merchant credit events/defaults.

5. Settlement, disputes, and recovery (after the payment)

Common risks: Chargebacks/disputes, ACH returns, and “friendly fraud” patterns that look like legitimate customer behavior until you zoom out across history.

6. Financial crime and compliance exposure

Common risks: AML red flags and related reporting/compliance obligations.

A quick way to prioritize

For each risk, score four dimensions (1–5 is fine):

Impact (loss size + fees + operational load)

Likelihood (frequency)

Speed (how fast it causes damage)

Customer friction risk (how likely a control will block good customers)

That last line—friction risk—is what connects payment risk management directly to growth and retention. Your goal isn’t “lowest fraud at any cost.” It’s lowest fraud with the highest approval rate you can safely maintain.

Prevention, detection, and response: the core layers

A workable program uses a layered security model. If one of the three layers is weak, the others get overloaded.

Layer 1: Prevention (reduce exposure up front)

Focus prevention on high-leverage moments—places where a small amount of friction prevents a lot of downstream loss:

Risk-based authentication for login, payment method changes, and refund destination changes

Limits and velocity controls (by user, device, account, instrument, and channel)

ACH-specific monitoring expectations: Nacha’s ACH Fraud Monitoring Requirements raise expectations for formalized procedures and continuous monitoring (with phased effective dates called out in CSG materials)

Layer 2: Detection (spot bad patterns fast—without over blocking)

Detection is where many programs break down because signals are split across payment rails and channels. Modern detection should aim for:

Cross-channel monitoring across ACH and cards, and across online/phone/in-person flows.

Near real-time alerting and decision support, so you can intervene before settlement cutoffs when possible.

Ongoing tuning as patterns evolve—because attackers adapt quickly, and static rules alone tend to either miss new fraud or spike false positives.

Layer 3: Response (make decisions consistently, at speed)

Response is not just “review the alert.” It’s a set of pre-approved actions with clear owners and SLAs, such as:

Auto-decline or auto-hold for transactions above defined thresholds

Step-up verification for suspicious but salvageable activity (to save good payments)

Void/cancel before settlement where applicable (especially when alerts arrive within operational windows)

Case escalation paths (front-line ops → fraud specialists → finance/legal/compliance as needed)

Building cross-functional ownership and processes

Payment risk management fails when it’s treated as “the fraud team’s job.” Fraud is a system issue spanning customer journeys, product decisions, data, and operations.

A practical ownership model usually includes:

Payments/Product: defines customer journeys, acceptable friction, and high-risk flows

Fraud/Risk Ops: owns strategies, rules/thresholds, investigations, and playbooks

Finance: quantifies loss, ROI, reserves, and chargeback/return exposure

Engineering/Data: instrumentation, data quality, model inputs, and integration reliability

Customer Support: closes the loop on false declines, disputes, and customer impact signals

Two processes make the biggest difference:

1. A rules/threshold change process (with guardrails)

Treat changes like product releases: request → evaluate expected impact → test/roll out → measure → iterate.

2. A documented escalation and decisioning process (with SLAs)

If you don’t define SLAs, your “response layer” becomes random:

Who decides?

How fast?

What happens if capacity is exceeded?

What’s the fallback (auto-approve, auto-decline, queue)?

Below is a straightforward example of an operational workflow you can copy: thresholds → monitoring → escalation → reporting → tuning.

Metrics and reviews that keep the program on track

If you only track fraud dollars, you’ll eventually “solve” fraud by declining too much good volume. Track balanced metrics in five buckets:

1. Loss and liability

Fraud loss rate (pre/post changes).

Chargeback and dispute rates (and $ impact).

ACH return rates (unauthorized/administrative/general).

Monthly: KPI scorecard (loss + friction + ops), plus a tuning plan.

Quarterly: risk appetite check-in (are you optimizing for growth, margin, or both?), plus a tabletop exercise for a major incident.

Where Payments Protection.ai fits (and why it’s relevant in consideration)

Once you’ve got the model, the question becomes: do you have the tooling and support to run it consistently?

CSG Payments Protection.ai is an AI-driven fraud detection and financial risk management solution designed to monitor ACH and card transactions across online, phone, and in-person channels, using an AI/ML-powered rule engine with custom thresholds to auto-decline, flag, and escalate cases.

It also supports a managed approach with CSG analysts for decisioning, plus periodic tuning and reporting.

It’s also positioned around outcomes that map directly to a growth-and-retention lens: reducing fraud losses while reducing false positives and customer friction, with KPIs like fraud loss rate, false positive rate, time-to-decision, and approval rate impact.

If you’re evaluating options, a practical next step is to run a short assessment using the framework above—then map your highest-priority journeys and risks to the controls, workflows, and KPIs you’ll need to operate at scale.

If you want to see how this model applies to your payment flows (and where you’re likely over- or under-controlling), explore CSG Payments Protection.ai and request a walkthrough focused on your channels, rails, and top fraud vectors.

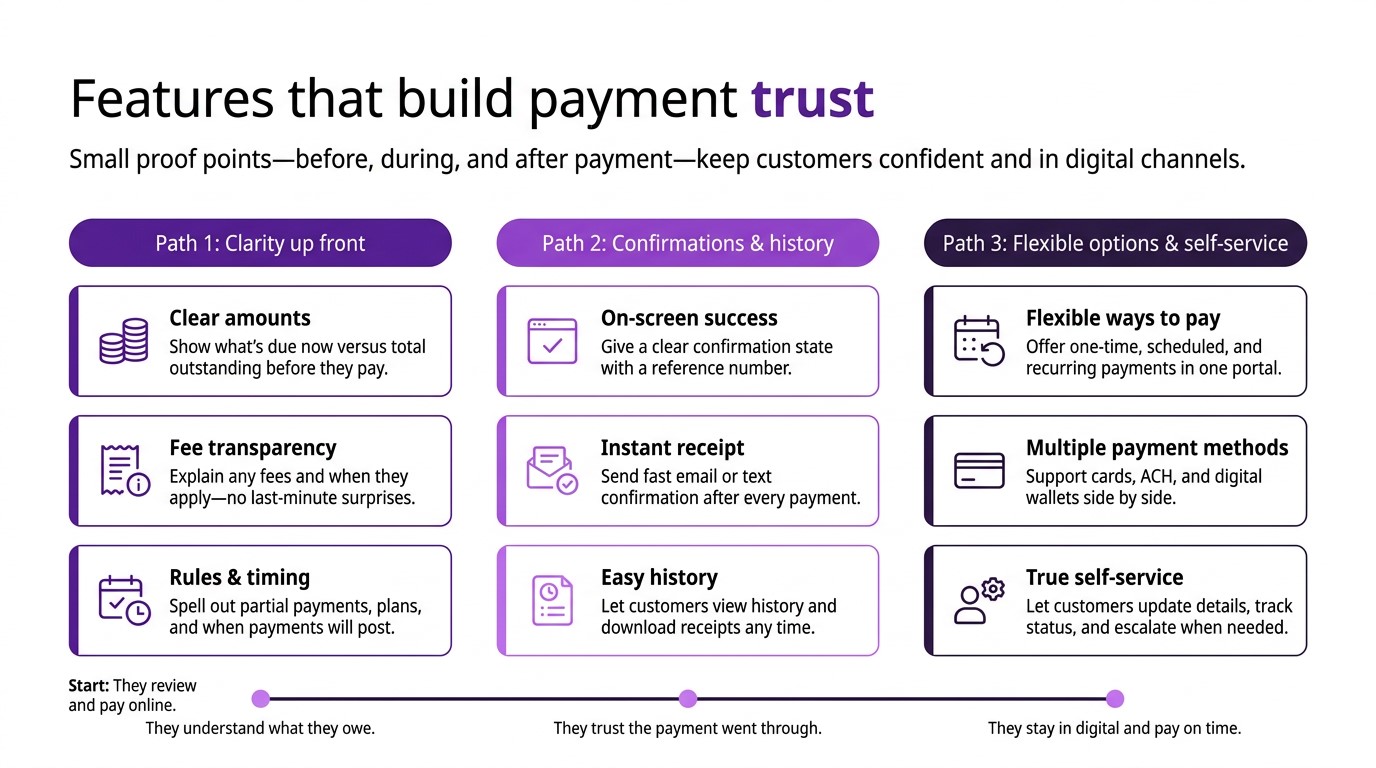

From Friction to Trust: How to Build a Safe, Smooth Digital Payment Experience

Posted on

Top Takeaways

Customers describe a “good” digital payment experience as fast, clear, and consistent—especially on mobile—rather than feature-heavy or flashy.

The most common friction points are forced registration, unclear amounts and fees, rigid payment rules, and self-service that can’t resolve billing or payment issues.

Organizations that simplify payment paths, add flexible options, and invest in true self-service see higher digital adoption, fewer late payments, and lower call volumes.

Subscription and recurring payment customers don’t wake up thinking about your payment portal. They just want to get in, pay what they owe, and move on with their day—without wondering if the payment actually went through.

When that doesn’t happen, you feel it as more late payments, more calls and emails, and more people standing at your counter because the “online system didn’t work.”

The gap between how organizations design digital bill payments and what customers actually want is still surprisingly wide. Instead of more complicated features, they’re looking for companies that simplify the flow, reduce friction, make options more flexible, and build trust with clear communication.

This article pulls together those patterns into a practical view of the digital payment experience from the customer’s side—and how you can turn that feedback into a real improvement roadmap.

How customers describe a “good” payment experience

When residents, patients, policyholders, or subscribers describe a “good” digital payment experience, they almost never talk about technology. They talk about how it felt.

Across customer research and portal performance data, three themes show up repeatedly.

1. “I can pay quickly, without hunting”

Customers want the path from “I got a bill” to “payment confirmed” to be obvious:

The “Pay now” option is easy to find on your site or in an email or text.

They can pay as a guest for simple, one-time obligations.

The number of screens and fields is minimal, especially on mobile.

The confirmation screen and follow-up receipt are clear and immediate.

In most contexts, when portals bury payment behind jargon-heavy menus or multiple redirects, abandonment goes up and people switch back to phone or in-person payments instead.

2. “I know exactly what I’m paying and why”

Most customers dislike surprises more than they dislike the amount due. A “good” digital payment experience makes the bill easy to understand:

Amount due and due date are prominent.

Prior balance vs. new charges are clearly separated.

Any fees, penalties, or rules (like partial-payment limits) are disclosed well before the final step.

The page explains when the payment will post and what happens next.

When fees show up late in the flow or balances are ambiguous, customers hesitate—or abandon the payment entirely.

3. “It works the same way, wherever I use it”

Consistency builds confidence. Customers expect:

Mobile and desktop experiences that behave predictably.

Buttons and forms that match familiar patterns (not custom experiments).

Error messages that explain what went wrong and how to fix it, rather than “something went wrong.”

Even small UX decisions—like preserving form entries after an error or using large tap targets on mobile—can be the difference between a completed payment and a frustrated call.

Where organizations overcomplicate payments

Most teams don’t set out to make payments hard. Complexity creeps in over time as policies, risk rules and legacy systems layer onto the customer journey.

Internal guidance for this pillar calls out several common mistakes.

1. Designing for edge cases instead of the main path

To avoid rare problems, many organizations over-validate every field, require multiple confirmation steps, or show every possible disclaimer for every customer.

The impact:

The majority of “normal” customers face extra steps.

Mobile users, in particular, see long forms and dense text they won’t read.

Completion rates drop, and more people end up calling instead.

A better approach is to make the happy path (standard bill payment) extremely straightforward, with clearly marked off-ramps or extra checks only when risk actually increases.

2. Using payments to achieve unrelated goals

Payments are a tempting place to collect extra data or promote new services. But adding non-essential tasks to the critical path—such as marketing opt-ins, lengthy surveys or cross-sells—often backfires.