What Are ACH Debits? ACH Debit Transactions Explained

Like many activities, financial transactions have gone digital. These electronic transactions occur primarily through an affiliated financial institution network called the Automated Clearing House (ACH) Network. This system helps move money between parties’ financial institutions simply, quickly and cost-effectively.

Nacha is that governing body that oversees the network and its transaction processing, which totals billions of dollars processed every year. Nacha establishes the rules and procedures for submitting and processing ACH debit and credit requests — the two main transaction categories. In 2020 CSG Forte was named a Preferred Partner for Government Agency ACH Payment Gateways by Nacha. This is a designation given based on leadership and innovation in advancing the ACH network.

What Is an ACH Debit?

An ACH electronic debit is a transaction withdrawing money from an account electronically. ACH debits can pull funds from checking and savings accounts, though restrictions on debits may apply to some business accounts.

Identification Requirements

Whether the transaction classifies as an ACH debit depends on which party originates the request.

For each debit, there’s a corresponding ACH credit — funds received by the other party to the transaction. When you authorize a company or individual to withdraw funds from your account electronically, they initiate the request with the network. These qualify as ACH debits since they’re pulling money from — debiting — your account. The funds’ ultimate deposit into their account represents the transaction’s ACH credit portion.

ACH Debit Payment Timing

While ACH debit payments and credits are swift, they’re not instantaneous. NACHA aggregates transactions and processes them in batches. Batches execute five times daily to facilitate efficient money transfers.

Advantages of ACH Debits

ACH debits for business have numerous advantages, including:

- Cost control: ACH debit processing is generally more affordable than handling physical checks or even credit or debit card transactions.

- Better risk mitigation: Since fewer people are involved in processing, there’s less fraud and error risk.

- Faster payment collection: ACH debits provide cash flow sooner than traditional check processing.

- Improved recordkeeping: Completing payments with ACH debits creates electronic traces for easier tracking, reporting and reconciliation.

- Environmental friendliness: ACH debits reduce the need for paper checks and mail trucks that consume resources.

- Reversibility: ACH debits can be reversed when errors occur, unlike wire transfers, which are generally challenging to recapture.

ACH Debit Challenges

ACH debits can also pose some unique challenges, such as:

- Financial institution restrictions: Some account holders restrict ACH debits to transactional, daily, weekly or monthly limits.

- Limited funds availability insight: The ACH network doesn’t support immediate feedback on errors or guarantee funds availability.

- Real-time execution: The ACH network doesn’t provide instant credits, though it can significantly reduce processing time versus physical checks.

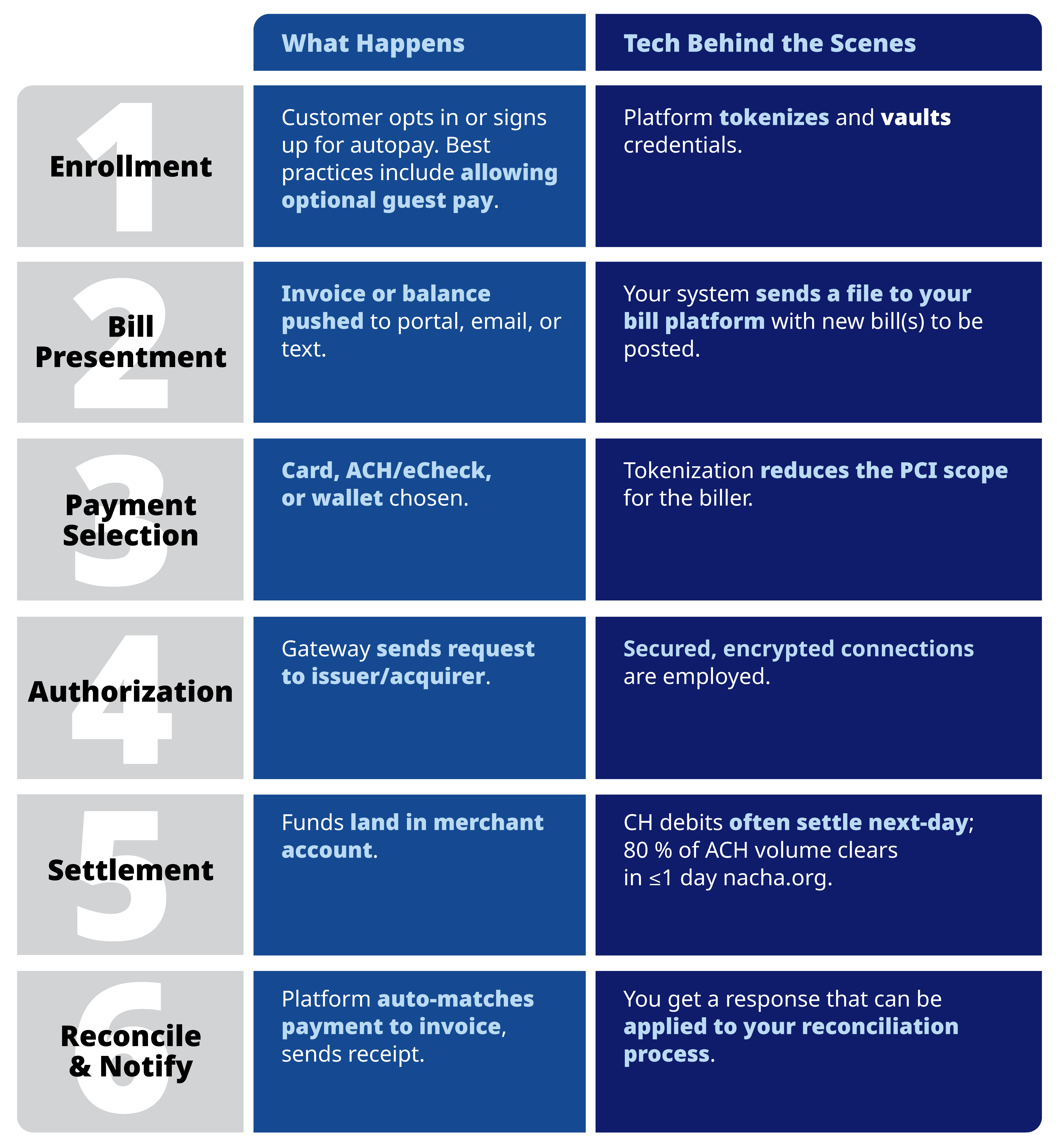

How Do ACH Debits Work?

ACH debits follow a prescribed three-step process:

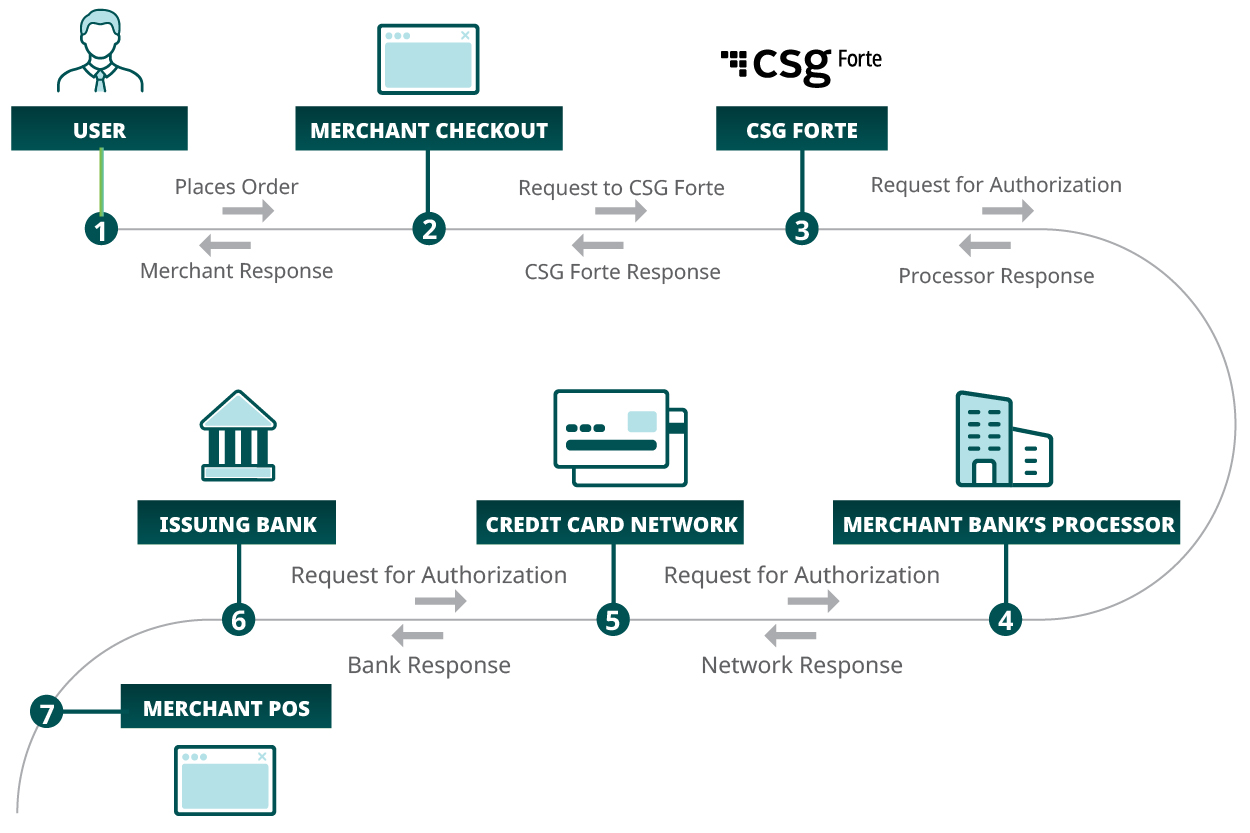

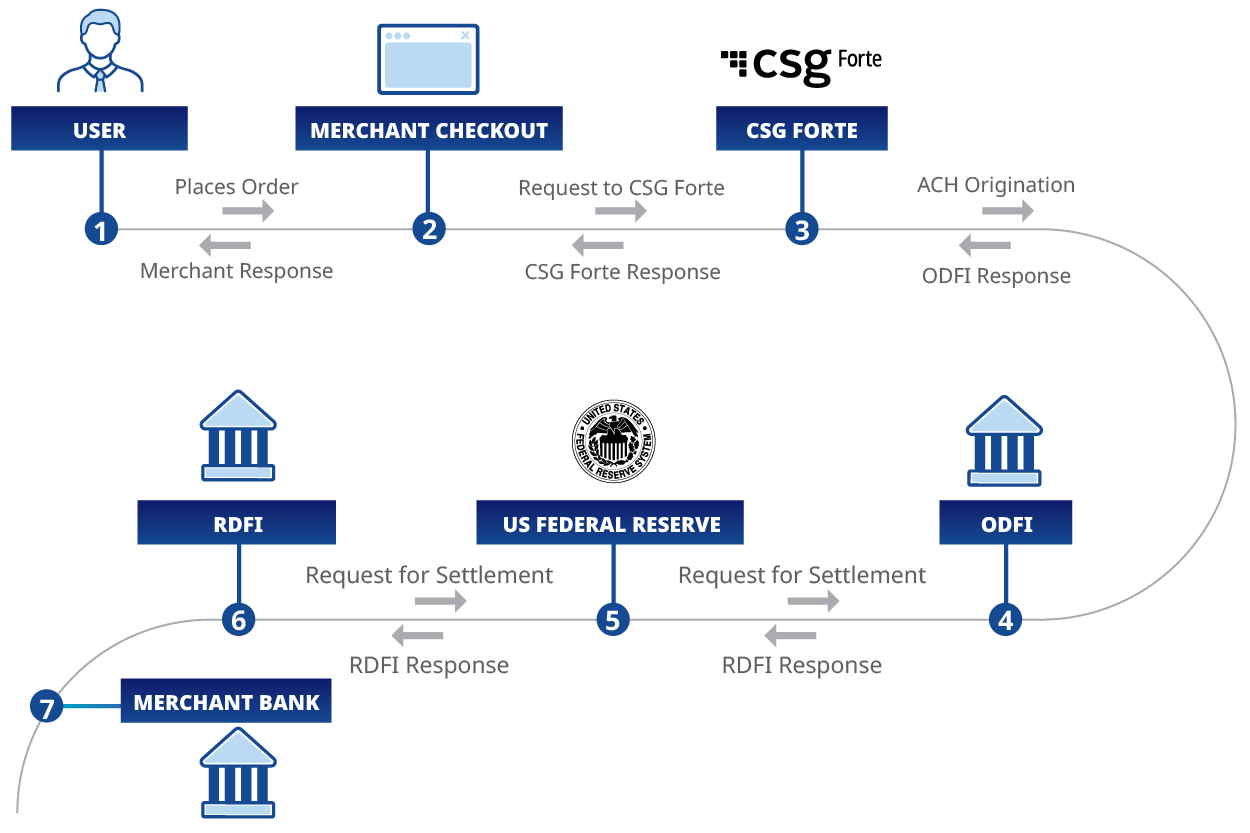

1. The payee initiates the request: The recipient submits a message to their account holder, called the originating depository financial institution (ODFI), requesting it to debit the payer’s account using:

- The bank routing and account numbers of the account to debit.

- The transaction amount.

- The Standard Entry Class (SEC) code.

- A proposed transaction settlement date.

The ODFI then enters the request on the ACH network.

2. The payer’s account holder receives the request: At regular intervals each business day, the ACH network passes these withdrawal requests to the payer’s account holder, the Receiving Depository Financial Institution (RDFI). The network bundles demand by institution, so the RFDI will get multiple debit requests with each “drop.” The RDFI investigates the requests and transmits any error messages or rejections to the ACH network.

3. The transaction settles: As long as there are no errors or rejections before the proposed settlement time, the ODFI and RDFI will transfer balances between each other through their respective Federal Reserve accounts. Once the ODFI receives the funds, it credits the payee’s account to finalize the transaction.

Main Types of ACH Electronic Debits

There are two primary categories of ACH debit transactions — recurring payments and one-time authorizations — before the activities receive additional standardized coding.

Recurring Payments: Establishing an automatic payment with a company gives it recurring authorization to initiate an ACH debit from your account information. For example, many consumers sign up for automatic payments on their wireless bills or streaming services. As the bill comes due each month, the provider uses the agreement to request the funds to satisfy the amount owed. This convenience ensures people don’t forget to pay and prevents late fees or service disruptions.

On-Demand ACH Transactions: One-time authorizations allow a receiving party to request the monies for a single transaction. They are also called on-demand ACH debits because they don’t represent an ongoing arrangement. An example is a consumer agreeing to an ACH electronic debit from their account for a tax payment or individual purchase. Under this ACH debit type, consumers generally retain more control over when a business can electronically withdraw funds.

Standard Entry Class Identification: The ACH network recognizes numerous debit types beyond recurring and on-demand. Initiators can use a three-character SEC code to identify the precise type.

- Accounts receivable entry (ARC): This code represents converting checks from payment drop boxes or mail into one-time authorization to debit the payer’s account electronically.

- Back-office conversion (BOC): BOC transactions use a check presented in person to initiate an ACH debit after acceptance.

- Machine transfer entry (MTE): This code applies to automated teller machine (ATM) withdrawals to debit a bank account for the funds withdrawn from the machine.

- Point-of-purchase transaction (POP): Unlike BOC check conversions, POP transactions use physical checks immediately upon receipt and return the paper check to the presenter once the system accepts the debit.

- Point-of-sale entries (POS): POS transactions may be the most common, as they use your debit card to withdraw the corresponding funds from your account.

- Prearranged payment and deposit (PPD): Recipients use this code to originate recurring and automatic payments.

- Shared network entry (SHR): Much like the MTE, the SHR code settles ATM withdrawals for machines within the same network.

- Telephone-originated request (TEL): This SEC identifier applies to payment authorizations received in phone interactions.

- Web-initiated transaction (WEB): As its name suggests, WEB is reserved for ACH debits agreed upon through internet activity.

ACH Debit vs. ACH Credit

ACH credits differ slightly from ACH bank debits, though they generally represent two sides of the same transaction.

A transaction qualifies as an ACH credit when an account holder electronically sends money to another’s account, typically at a different financial institution. Since they’re depositing funds rather than withdrawing them, this action is also called a “push.”

The ODFI will enter the request with ACH, which passes the crediting information onto the RDFI. Settlements occur the same way as with ACH debit — as long as the information reconciles correctly, the RDFI accepts the funds and credits the recipient’s account.

Direct deposits, electronic refunds and peer-to-peer payments are all ACH credit transaction examples.

EChecks vs. ACH Debit

eChecks — short for electronic checks — can represent an ACH debit, but the term isn’t definitive. While eCheck can describe any portion of the digital money exchange, ACH debit applies specifically to cases where the recipient initiates the payment request.

Another key difference is whether the money transfers via ACH. eChecks can be used to support a wire transfer that occurs outside the ACH network. Almost all physical checks go through some electronic processing, but not all result in ACH debit and credit transactions.

Choose CSG Forte as Your ACH Debit Solution

As an experienced NACHA Preferred Partner for payment solutions, CSG Forte leverages scalable, easy-to-use technology to simplify and streamline online payment collection.

Contact us to request a personalized quote, or apply for your account today.