Secure, Swift, Seamless: Why Your Customers Love Digital Wallets

Posted on

Consumers want fast, convenient ways to pay for their purchase—without digging through their wallet for their card payment details. Shoppers increasingly say they choose where to shop based on how convenient the online payments process is. One way to enhance your customer experience (CX) and streamline the online transaction process is by offering your customers digital wallets as a payment option.

Digital wallets are gaining popularity—with an expected 5.3 billion users by 2026. They’re becoming increasingly important not just for the benefits they provide customers; businesses that take advantage of this evolving technology soon will be ahead of the game—digital wallet adoption still lags among some types of merchants, despite continued increase in consumer usage.

It’s those ongoing advancements in digital wallets that are exactly why collaborating with a knowledgeable payments provider is essential for organizations that want to attract and keep customers in a dynamic online payment environment.

The Rise of Digital Wallets

Digital wallets are becoming mainstream. They’ve transcended novelty status and become an integral part of everyday life. Consider this: 79% of Gen Z consumers use digital wallets at least once a month. They’re also growing in popularity with Millennials and Gen Xers, half of whom reported using digital wallets more often than traditional payment methods in a recent Forbes survey.

So, we know digital wallets are increasingly popular. But, why?

Customers Expect Fast, Secure, Streamlined Service

Customers crave simplicity. They want transactions to be swift and secure, and they don’t want to take any unnecessary steps. Digital wallets fulfill these expectations by offering:

Fast Processing: With a few simple steps, payments are completed in seconds.

Security: Digital wallets employ robust encryption and authentication methods, providing peace of mind for users.

Reduced Redundancy: Say goodbye to repeatedly entering card details—digital wallets store payment information securely.

Why Offer Digital Wallets?

Meet Customer Expectations

Customers expect to see familiar payment options when they visit your website. Digital wallets have become a standard feature for most consumers, akin to credit cards and bank transfers. By offering a digital wallet option, you signal that your company is attuned to consumer preferences and up to date on the latest technology.

Increase Trust and Security

Trust is the bedrock of any successful business relationship. Customers recognize digital wallets as secure payment methods. Whether it’s PayPal, Venmo, Apple Pay or Google Pay, these platforms have earned their reputation for safeguarding sensitive data. By integrating them into your payment ecosystem, you reinforce trust with your audience.

Streamline the Checkout Process

Offer a frictionless checkout experience: no fumbling for credit cards, no manual data entry. Digital wallets eliminate these pain points. Customers appreciate simplicity—they can complete purchases swiftly, especially on mobile devices. This simplicity also helps your company’s bottom line; consumers who use digital wallets spend 31% more than non-users, according to recent survey data.

Choosing the Right Payment Methods

Quality Over Quantity

While variety is enticing, overwhelming customers with too many payment options can backfire. Instead, focus on quality. Prioritize widely used digital wallets that resonate with your audience. Remember, simplicity is best.

Understanding Customer Preferences

Knowledge is power. By analyzing transaction data, you can discern which payment methods your customers prefer. Do they browse from Apple devices? Then consider offering Apple Pay. Are they connecting using Google Chrome? Google Pay may help you speed up transactions. Armed with this type of insight, you can tailor your offerings and enhance the user experience.

Collaborating with Payment Providers

Now, let’s address the elephant in the room: managing separate accounts with various digital wallet providers. It’s time-consuming and inefficient. Here’s where a payment provider comes to the rescue:

Centralized integration: Partnering with a payment provider allows you to consolidate digital wallet options. Instead of juggling multiple accounts, you have a unified interface.

Seamless updates: When a new digital wallet emerges or an existing one evolves, your payment provider handles the integration and is there to guide you through the process.

Efficiency: Focus on your core business while the payment provider manages the technical intricacies.

Remember, the goal is to enhance your customers’ experience. By offering digital wallets and collaborating with a reliable payment provider, you’re not just streamlining payments—you’re building trust and loyalty.

The future of wallets is digital, and now is the time to claim your spot—ahead of the competition. Incorporating digital wallets isn’t a trend, it’s a necessity to stay relevant and keep customers coming back. Your customers demand speed and convenience; meet their needs by adopting digital wallet technology today. Contact our experts at CSG today.

PCI Compliance Guide

Posted on

Payment card industry (PCI) compliance is the global security standard for organizations that accept consumer credit card payments. Being PCI compliant entails adhering to a variety of best practices, security measures and benchmarks that determine how you collect and store customer information while processing transactions. Let’s break down what you need to know about PCI compliance and its primary benefits. We’ll also outline how your organization can streamline the process of achieving PCI compliance.

What Are PCI Standards and Compliance?

PCI compliance comprises the technical and operational requirements your business needs to follow to protect consumer credit card data. It’s a comprehensive set of policies ranging from regular system upkeep to clearly delineated user permissions.

The PCI Security Standards Council develops and manages compliance standards to help organizations fortify their security systems and prioritize consumer data protection.

PCI compliance requirements include:

Security against malicious software

Routine network maintenance

Cardholder data encryption

Restricted internal access to sensitive data

PCI Credit Card Compliance Overview

PCI compliance may seem challenging if you are unfamiliar with the terminology or the latest cybersecurity best practices. But you don’t have to figure it out alone. You can achieve compliance and minimize risk by partnering with a trusted, experienced payment service provider. The PCI Security Standards Council provides a list of approved Qualified Security Assessors (QSA) companies you can reference for easier navigation. Still, it is valuable for your business to grasp the fundamentals of PCI compliance. Here is an overview to get a better understanding:

It’s a continuous exercise: PCI compliance is an ongoing process that your organization should review yearly.

Your payment methods have an impact: The type of payment services you offer can affect the amount of work you need to do to remain compliant.

Requirements vary: Your compliance requirements depend on the size of your organization and the number of card payments you process annually.

Your transaction count matters: PCI compliance rules sort businesses into several groups. Level-one merchants have the most requirements to meet because they process over six million annual transactions across channels. Smaller organizations will have fewer transactions, and therefore fewer rules to follow.

Merchant account providers may add requirements: To accept credit card payments, you need a merchant account and service provider. If you have a merchant account, your payment service provider should have PCI compliance-related requirements included in the terms and conditions of your agreement.

The Primary Goals of PCI Compliance

The principles that guide the 12 PCI requirements can be summarized in six main goals:

Build and maintain a secure network and systems: Use strong passwords, firewalls and/or software security technology to protect your network from hackers.

Protect account data: Keep your customers’ data safer with encryption, tokenization and other ways to disguise sensitive information.

Maintain a vulnerability management program: Establish a vulnerability management program that helps protect your organization from malware.

Implement strong access control measures: Restrict which employees can access cardholder information. Ensure limited users have access in person and online.

Regularly monitor and test networks: Test your networks regularly and track who is accessing cardholder data.

Maintain an information security policy: Your staff must be familiar with internal procedures and regulations regarding cardholder data.

The 6 Compliance Groups for PCI DSS

Organizations that must adhere to the PCI Data Security Standard (DSS) fall into one of six categories. These categories depict the organizations’ level of involvement in card data handling and conducting card transactions. The six groups are:

Merchants: Businesses that directly accept customer card payments are merchants. All merchant organizations must comply with PCI standards to prevent security breaches and protect cardholder information. Merchants must ensure secure card environments, including those related to data transmission, physical security and access control measures.

Service providers: Entities that transmit, store or process data on a merchant’s behalf are service providers. These organizations may include security service companies, payment gateways or hosting providers. Organizations in this category must demonstrate compliance to merchants and adhere to PCI DSS.

Qualifies Security Assessors: QSAs are independent entities that assess service provider and merchant compliance with PCI DSS. These organizations verify security measures and their effectiveness.

Internal Security Assessors (ISAs): ISAs refer to internal employees of PCI Security Standards Council-certified organizations who have the training to assess and validate organizational procedures, policies and security controls.

Payment card brands: Major credit card companies, including Mastercard, American Express and Visa, fall into this category. These entities establish the guidelines and security requirements for protecting cardholder information. They can impose penalties, such as fines, on merchants that fail to adhere to standards or practice malicious compliance.

Acquiring banks: Financial institutions that craft agreements with merchants to process card transactions are considered acquiring banks. These organizations aim to ensure merchant compliance with PCI DSS to minimize fraudulent activity and similar adverse outcomes that could tarnish the organization’s brand or reputation. Some acquiring banks require merchants to undergo regular security audits or provide compliance evidence to ensure ongoing standard adherence and best practices.

12 Requirements for PCI Compliance

The PCI Security Standards Council provides 12 requirements for businesses to be compliant. Here is an overview of the PCI DSS requirements:

Goal: Build and Maintain a Secure Network and Systems

Install and maintain network security controls: Install and update a network security device or software-defined technologies that check traffic entering and exiting your network, identifying and blocking potential cyber threats. Test your networks and control connections to untrusted networks.

Apply secure configurations to all system components: You must define and implement processes and mechanisms that ensure the secure configuration and management of system components. For instance, you may do this by changing vendor-supplied passwords, restricting generic settings, removing functionality where necessary, encrypting access or enabling only essential services.

Goal: Protect Account Data

Safeguard stored account data: Protect payment data. Implement policies for disposing of cardholder data, avoid storing sensitive data and limit what you keep, which should be strictly what is necessary for the needs of the business.

Protect cardholder data with strong cryptography during transmission over open, public networks: Do not send unprotected account numbers (PAN) and sensitive personal information by any end-user communication technology. Instead, use strong cryptography.

Goal: Maintain a Vulnerability Management Program

Protect all systems and networks from malicious software: Put mechanisms and processes in place to protect your networks and systems from malicious software and malware. Equip your staff with mechanisms to protect them from phishing attacks.

Develop and maintain secure systems and software: Spend time reviewing vulnerabilities and risks, then implement processes and systems to provide protection, including following secure development and coding practices.

Goal: Implement Strong Access Control Measures

Restrict access to cardholder data by business need-to-know: Restrict cardholder data to only users who need to use the information to complete transactions. Define access roles, privileges and controls so only authorized users can access data.

Identify users and authenticate access to system components: Authenticate users and document policies, and see that each user has unique, identifying credentials. For a production environment where you store account data, you must implement multi-factor authentication.

Restrict physical access to cardholder data: Mechanisms to restrict access to cardholder data must be in place. For instance point-of-sale devices must have protection from tampering or non-authorized substitution.

Goal: Regularly Monitor and Test Networks

Log and monitor all access to system components and cardholder data: Ensure your system has an audit trail, and leverage time-stamped tracking tools. These tools can show you when employees access data and help you review logs and identify suspicious activity.

Test security of systems and networks regularly: Test and catalog wireless access points. Schedule frequent security vulnerability assessments and proactively monitor traffic.

Goal: Maintain an Information Security Policy

Support information security with organizational policies and programs: Establish, publish, and share your company’s information security policy. Explicitly state rules for technologies, key responsibilities and best practices. Give new employees the policy once they sign on. Consider that education on security awareness must be an ongoing activity.

Payment service providers help you manage PCI compliance, making the 12 requirements and six goals simple for you to oversee. Robust platforms will have many of the rules built in, automating the process. The bottom line is that you do not have to go at it alone.

Note on PCI DSS V4.0

March 2024 marked the beginning of PCI DSS version 4.0 application. Full implementation of PCI 4.0 requirements became effective in March 2025. The latest version of the standard includes many changes that you can check here. A summary of some of the reasons for the changes comprise:

Evolution of security needs: As threats evolve, security practices must evolve as well. That is why PCI DSS V4.0 includes requirements for multi-factor authentication, password updates and e-commerce and anti-phishing.

Security promotion as a continuous process: To face ever-changing malicious conducts, you need to keep a recurring, well-defined and strong policy and processes.

Increase flexibility to achieve security objectives: Your organization may adopt an innovative or different approach to achieve some objectives while maintaining strict controls and processes and keeping the security objectives at the core of your planning and execution.

Enhance procedures and validation methods: Achieve transparency and granularity by designing for clear validation and aligned reports.

How to Achieve PCI Compliance

To become PCI compliant, you need to meet the requirements, do an assessment and complete a security scan:

Meet the requirements: Your organization must comply with the PCI Security Council’s rules and any amendments to provisions and sub-requirements.

Complete an evaluation: Your organization should complete an assessment showing your security systems and measures to safeguard consumer information. Smaller organizations may complete a self-assessment. Larger enterprises must use third-party auditors to assist.

Perform a security scan: Your organization must scan the network you use to process payments. The scan is highly specialized and technical and benefits from expert assistance from an independent firm.

Organizational PCI Levels of Compliance

For PCI compliance, your organization must undergo a rigorous annual assessment. Although the requirements are universal, your business may need to adhere to additional rules and undergo more stringent checks. Depending on the size of your organization and the amount of transactions you process annually, you will fall into four main categories:

Level-one organizations: If you process more than six million Visa payments annually across various channels, you fall into level one. You will have the most robust assessments and rules you must adhere to.

Level-two organizations: Level two organizations complete between one and six million Visa transactions yearly.

Level-three organizations: If you process between 20,000 and one million Visa payments every year, you fall into level three.

Level-four organizations: Level four organizations process under 20,000 Visa transactions each year.

PCI Security Standards Council may move organizations that have experienced a cyberattack resulting in data loss into a higher validation level—regardless of the yearly transaction amounts.

The Benefits of Credit Card PCI Compliance

Your organization benefits from continuously evaluating and maintaining your security systems and addressing gaps. Other benefits of being PCI compliant include:

Minimizing the risk of data breaches

Protecting cardholder data

Reducing the risk of consumer identity theft

Identifying, monitoring and addressing security vulnerabilities

Decreasing the risk of paying fines associated with data breaches

Safeguarding your organization’s reputation

Keeping customers happy and confident when transacting with you

Frequently Asked Questions About Credit Card Compliance

Have more questions? Here, we’ve answered some frequently asked questions about PCI compliance and related terms or processes.

1. Who Must Be PCI Compliant?

If your organization accepts, transmits or stores cardholders’ personal data, you must be PCI compliant.

2. What Does PCI Compliance Mean?

PCI compliance means that your organization meets the various security requirements that the PCI Security Standards Council provides. Meeting this compliance means the way your organization accepts, transmits and stores data is safe, private and secure according to the PCI mandate.

3. What Is the Definition of Malicious Compliance?

Malicious compliance, when relating to PCI, refers to situations in which a company appears to adhere to PCI standards but intentionally implements strategies with minimal effectiveness. Organizations that practice malicious compliance often leave significant vulnerabilities. These attempts to appear compliant without truly securing sensitive information aim to deceive customers, clients and entities.

Examples of malicious compliance could include weak encryption, non-functional security controls or insufficient access controls. Organizations practicing malicious compliance could face severe penalties.

4. Is PCI Compliance Required by Law?

PCI Security Standard Council monitors the implementation of standards. PCI SSC standard is at the discretion of organizations that manage compliance programs, such as a payment brand, acquirer or other entities.

5. How Do I Become PCI-Compliant?

PCI compliance is achieved by completing a self-assessment questionnaire (SAQ) or hiring an approved vendor third-party auditor to complete the assessment, CSG Partners with Aperia, a QSA Approved Vendor. Upon completing the SAQ and vulnerability scan (if applicable), submit all documentation and evidence to your payment processor (CSG Forte).

6. What Are Examples of PCI Compliance and Data Breaches?

When there are large PCI violations and data breaches it is often newsworthy. The sheer volume of the data and the high profile of the companies involved make these events prominent in the public eye, harming brands’ reputations and exposing millions of consumers to theft and identity fraud. However, it’s key to remember that cybercriminals target companies of all sizes and industries and no business is immune.

7. What Can My Business Do to Simplify PCI Compliance?

Although the technical aspects of completing the PCI assessment may be beyond the scope of what you can do yourself, your organization can take steps to make the process easier. Focusing on data hygiene is a good example. Here is a PCI compliance checklist:

Ensure your organization uses strong passwords and has strict protocols to enforce this.

Keep your software updated.

Only store the data you need.

Be wary of links—encourage employees to think twice before clicking on suspicious links.

Explain to employees the importance of protecting consumer data and the implications of not doing so.

Meet PCI Requirements With CSG Forte

Boost your payment security and protect customers’ sensitive data with CSG Forte’s secure payment solutions. Leverage the industry’s highest security standards with a platform with built-in PCI compliance mandates. CSG Forte provides:

Secure payments: Keep your consumer data safe with every transaction with CSG Forte’s advanced technology standards and protocols.

Tokenization: Leverage randomly generated tokens with no intrinsic value to replace cards, automated clearing house (ACH) networks and other sensitive data. Tokenization helps your organization safeguard against digital security breaches.

End-to-end encryption: Using PCI-validated end-to-end encryption, you can disguise credit card data during transmission. The encryption ensures card data is valueless if intercepted.

Hosted payment pages: Make sure your organization never stores data in your system using hosted payment pages (HPPs) or external checkout pages. CSG’s platform enables you to provide secure checkouts that won’t require you to manage and collect sensitive data during transactions. Third-party checkout is the easiest, most popular and safest way to accept online payments.

Adherence to compliance standards: Benefit from adhering to the most robust, reliable and up-to-date compliance programs. CSG’s security and compliance experts focus on delivering solutions in compliance with various mandates. We hold ISO 27001:2013 certification and maintain PCI DSS v3.2.1 compliance and Health Insurance Portability and Accountability Act (HIPAA) compliance. We deliver SSAE 18 / ISAE 3402 SOC 1 Type II reports to ensure your organization’s credibility, accuracy and system security in safeguarding consumer data.

Streamline Your PCI Compliance Requirements

Protect consumer data and prioritize security by leveraging CSG Forte’s award-winning payment platform. Our easy-to-integrate and navigate solution streamlines your payments, helping you process your transactions in one place.

Meet PCI compliance requirements with our built-in functionalities and tools, simplifying secure transactions. Build consumer trust and have peace of mind knowing your payment systems are robust and leveraging the latest security technology.

For over two decades and counting, CSG Forte has been helping thousands of government, insurance, telecom and other industry merchants optimize security, scale their business and process omnichannel payments efficiently.

Whether you are a new merchant or an existing merchant, we can help you achieving PCI compliance and get the support you need to ensure processing payments is a frictionless endeavor. Contact our team.

What Are eChecks? Questions About eCheck Payment Processing Answered

Posted on

The payments industry is undergoing a digital revolution—electronic payments are becoming the norm, and traditional payment methods are decreasing in use. Electronic checks (i.e., eChecks) are one of the increasingly popular digital payment methods.

An eCheck allows users to withdraw money from a checking account and deposit it digitally into another account, with no paper required. In 2003, the Check Clearing for the 21st Century Act (Check 21) established the regulations for eCheck payment processing. As a result, eChecks are a quick, secure and convenient digital payment method.

In this blog, we answer the most common questions about eChecks. Review our answers to learn more about electronic checks, their benefits for your business and how you can start accepting eChecks today.

1. What Is an eCheck?

An eCheck is a digital check that allows users to make an electronic payment from a checking account. Like a paper check, an eCheck requires the user to input basic personal information, but the information is collected electronically, and the transaction is processed entirely online.

The electronic check payment withdraws money from a payer’s checking account, transfers the funds via the automated clearing house (ACH) network and makes an eCheck deposit in the payee’s checking account using a payment processor.

People can use eChecks to pay companies for one-time or recurring bills. Businesses with an ACH merchant account can withdraw a customer’s payment directly from their bank account with the customer’s authorization.

eChecks are most beneficial to these types of businesses:

Businesses accepting large payments: For high-value payments, eChecks help you save money. eCheck processing involves fewer parties than credit card payments and avoids interchange fees.

Online companies: Since online businesses already operate digitally, they can collect payment details online for eCheck payments.

Subscription-based businesses: Since eChecks are a type of recurring payment, customers can set up their account to send an eCheck on a repeating basis. Recurring eChecks are convenient for customers and businesses. Customers will always pay their bill, so the company will receive payment on time every period.

Other common names for eChecks include direct debit, online check and internet check.

2. How Does an eCheck Work?

An eCheck works like a paper check, except the information is transmitted electronically, making the process more efficient. eCheck payments require these steps:

The customer starts a transaction: A customer authorizes an electronic money transfer by initiating an eCheck to a company for goods or services. Merchants must obtain permission from the customer through a contract, order form or similar method to withdraw money from their checking account.

The merchant collects the payment details: Once the merchant has received customer authorization, they can collect the details needed for the eCheck, such as the customer’s bank account and routing numbers. Merchants can ask for this information via an online form, a paper form or over the phone. For recurring payments, the customer and merchant must decide on a payment schedule.

The payment processor verifies the details: The merchant enters the customer’s details into the payment processing software. The merchant’s payment processor will validate the eCheck details to ensure the transaction is legitimate. Funds are verified 24 to 48 hours after the customer starts the transaction.

The merchant’s account receives the payment: After verification, the ACH network will process the eCheck. The funds will move from the customer’s account to the merchant’s account within a few business days. Once paid, the customer will receive a receipt to confirm the eCheck has been deposited successfully.

3. What Payments Can Be Made With eChecks?

You can use an eCheck to make many types of payments. Rent, utility bills, business invoices and mortgage payments are all payable with eChecks. You’ll also see eChecks used for tuition payments, online purchases and nonprofit donations. Essentially, any transaction you can make with a paper check is payable with an eCheck. eChecks just make paying with checks more convenient since you can pay them from anywhere.

eChecks are common for several types of payments—especially those that are high-cost—such as:

Mortgage payments

Rent

Car loan payments

Utility bills

Fitness memberships

Legal retainer fees

Subscription fees

Check with the institution or business you’re paying with a paper check to see if they’ll take an eCheck instead.

4. How Are eChecks Different from Other Electronic Payment Methods?

The payment industry uses several terms for money transfers, and each term means something different. Payment types that are similar to, but not the same as, eChecks include:

EFT: An electronic funds transfer (EFT) is a general term for electronic payments, such as eChecks, wire transfers and direct deposits.

Paper check: A paper check is a slip of paper where customers write out payment details. They give this paper to the merchant, and the merchant uses the paper check to withdraw funds from the customer’s account. An eCheck is essentially a digital form of a paper check.

ACH: ACH and eChecks both transfer funds between bank accounts. eChecks use the ACH network to make transfers and manage funds between the payer and payee accounts.

Credit card: eChecks and credit cards both process electronic payments, but in different ways. eChecks use the ACH network to transfer funds. Additionallly, they have low processing fees and no credit card interchange fees. Credit cards use their own payment infrastructure to process payments, resulting in higher fees.

Wire transfer: A wire transfer manually moves funds from one bank account to another. Wire transfers are more costly since they’re manual. They’re also less secure since payments cannot be revoked.

To understand these differences, you could say eChecks are a type of EFT that acts like a digital version of a paper check, using the ACH network to process payments quicker and cheaper than credit cards or wire transfers.

5. Are eChecks Secure?

eChecks are generally a safe form of payment. Working with a trusted platform provides security support through encryption and authentication processes. The ACH is also a highly regulated and secure network, further protecting personal and proprietary information. Banks and payment processors use fraud detection and tokenization to decrease risk levels; however, any financial transaction carries a potential fraud risk. That’s why merchants and customers should only work with reputable businesses on secure networks. Remember to keep an eye on your account activity and report unusual activity immediately to catch security risks early.

Security is the primary advantage of eChecks over traditional payment methods because they are subject to consumer protections codified in Regulation E, federal law that protects consumers against fraudulent and incorrect EFTs. The security components of electronic check payments include:

Authentication: Authentication verifies the identity of the individual who’s submitting account information. This process ensures that the merchant gets legitimate payment information and the customer consents to have funds taken from their account.

Digital signature: A digital signature is an encryption technique that uses timestamps to ensure eChecks cannot be duplicated.

Duplicate detection: Duplicate detection monitors eCheck transactions for suspicious activity. This strategy can detect fraud, such as duplicated checks.

Encryption: Encryption masks payment data to make it nonsensitive. Encrypted data is useless if stolen because the hacker must have the encryption key to decrypt the information. All ACH transactions, including eChecks, must be encrypted if they occur over unsecured electronic networks.

Public key cryptography: This step is part of the encryption process. The key has the information needed to encrypt data during the transfer and cipher it at the receiving bank.

Certificate authorities: The certificate authorities store, sign and issue a digital certificate to encrypt transactions, secure communication and protect information. They can certify the ownership of a public key. A Secure Sockets Layer (SSL) certificate is an example.

6. What Are the Benefits of eChecks?

eChecks offer several benefits for businesses and customers. Besides being a secure payment method, companies should take advantage of eChecks because they:

Process faster than checks: eChecks take only three to five business days to finalize since the transaction is completed online. This timeline is much faster than paper checks, which can take more than a week to finalize while the payment details are verified. With eChecks, you’ll get paid right away instead of waiting for your money.

Increase revenue: Accepting eCheck payments can help your business make more money. Checking account numbers stay the same, whereas credit card numbers often change, so your payments will go through more often, with fewer chargebacks. eChecks can also be set up as recurring payments, ensuring you get paid on time and eliminating the need to track down paper checks.

Save money: eChecks have lower processing fees than credit cards. By accepting eChecks, your company can pay less in fees and get more money for your operations.

Are easier to track: Hard copies of payment confirmations take up physical room in your office. With an eCheck, you and your customers will receive an email confirmation of payment, which you can store digitally.

Cannot be lost or misplaced: An eCheck is a digital record, so it’s virtually impossible to lose. The banks and ACH network will keep track of the payment until it’s processed. Paper checks can be lost, requiring the payer to issue another check and stop the original check to prevent someone else from cashing it.

Reduce waste: Since eChecks exist digitally, no paper is required. Your business can use less paper and reduce waste.

7. How Long Do eChecks Take to Process or Clear?

eChecks will usually take two to five business days to clear. The exact timing depends on how the bank and ACH network handle the transaction. This process takes several days while the eCheck is verified and cleared, delaying the fund transfer. Using credit or debit payments is instant; eChecks take more time, but are still faster than physical checks.

8. Do eChecks Process on Weekends?

eChecks will not process on weekends. eChecks rely on the ACH network to complete the transaction. The ACH network follows the traditional workweek, meaning you’ll need to work within a Monday-to-Friday schedule. Any eChecks initiated on Fridays or during the weekend will wait for processing until the following Monday. Keep this in mind when planning your time-sensitive payments—try to get your eChecks in early to avoid weekend delays.

9. How Much Does It Cost to Process an eCheck?

eCheck processing costs will vary based on the institution. The exact fee will usually be a small percentage of the transaction total. Additionally, there might be a monthly fee attached to your account. Some banks and payment processors charge additional monthly fees to cover costs. However, you might see a smaller processing cost for larger orders. Despite their processing costs, it’s often cheaper to use eChecks than credit cards, which usually carry higher processing fees.

10. How Do I Send an eCheck Payment?

To send an eCheck, you’ll most often use an online form to input your bank routing number and account number. Once you have entered the correct information, you can initiate your eCheck payment through your bank or payment platform. You’ll type in the essential transaction details and send your eCheck off to process. Once the processing period is over, the funds will be transferred from your account.

11. What if an eCheck Bounces?

If your eCheck bounced or is returned, it means there weren’t enough funds in the account. If you’re dealing with this issue, you must contact the sender to get the amount paid correctly. If you’re the sender, make sure your account has enough funds to cover the check. If it does not, add the funds you need and try to resend the check. If you have enough funds in the account, there could be a problem with the recipient’s information. Double check everything and contact your bank for assistance.

If you’re the eCheck recipient, you’ll need to invoice the sender again or ask for a different payment method. Some banks and processors may charge a fee for bounced eChecks, so check your account for additional charges.

12. How to Cancel an eCheck

Canceling an eCheck is straightforward if the check hasn’t cleared. If you need a check canceled, contact your bank or payment processor as soon as possible. Try to reach out within the same day to prevent the check from clearing. If the eCheck still needs to clear, the bank can usually stop it from being processed. However, once the process starts, check cancellation is probably impossible. You’d need to contact the recipient and request the funds be returned. Always check the information on your eChecks for accuracy before sending them.

13. Can Customers Submit Chargebacks on eChecks?

Yes, customers can submit chargebacks on eChecks. The process is different from credit card chargebacks. With eChecks, you’ll see chargebacks due to insufficient funds, processing errors or unauthorized transactions. Customers have to contact their bank to start the chargeback. Once they do, they can reverse the transaction. However, customers need to file their disputes within a set time frame—otherwise, the chargeback will not go through.

14. How Can I Get an eCheck Merchant Account for My Business?

Getting an eCheck merchant account starts with contacting your payment processor for ACH services. You’ll need to give them your business information—like tax identification, transaction details and financial statements. If you’re approved for an eCheck merchant account, you can start accepting eChecks from senders. If you’re denied, you’ll need to work with the payment processor to find out what you need to do to get approved.

15. What Are Some Common eCheck Challenges?

While eChecks are a convenient payment format, they can come with some challenges. You should be aware of these potential problems before using eChecks:

Processing delays: Processing time is one of the main eCheck challenges. Waiting several days for a check to clear can affect your access to funds. While credit and debit transactions happen instantly, you’ll need to wait for eCheck processing to finish. These delays might affect your cash flow, disrupting your business.

Fraud risks: eChecks are fairly secure; however, there fraud risks are always present. Compromised bank account details can lead to unauthorized transactions, for example. Banks have protections in place, but becoming a victim of fraud can be stressful and time-consuming, and recovery can be arduous and complicated. Always ensure you’re using a secure payment platform to protect your sensitive information.

Bounced or returned echecks: eChecks can bounce just like paper checks. If the sender lacks the funds, checks will not go through. Failed transactions mean delays and potential fees for the sender and recipient. Businesses dealing with bounced checks will have to follow up with the customer to get the problem fixed, which will delay the transaction even more.

Limited support: While eChecks are convenient, not all businesses accept them as payment. If you want to offer eChecks, you’ll need to find a provider that supports ACH transactions. Getting eChecks set up could involve additional costs.

Customer adoption: Some customers might avoid adopting eChecks over information concerns. Not everyone wants to share their bank information online. This concern can limit the adoption of eChecks for customers, especially if many of your customers prefer credit cards. Educate your customers about eChecks to encourage them to adopt the new payment method.

CSG Forte Can Help You Accept eChecks

Your company needs a payment processor to accept eChecks from your customers. CSG Forte can help you start processing eChecks on our trusted payments platform. Our software solutions allow merchants like you to accept eChecks, ACH payments, credit cards and debit cards. Reach out to us today and see how we can simplify your payments processing!

Not Ready for Rising Card Fees? Try These 4 Payment Alternatives

Posted on

Credit cards emerged from the pandemic stronger than ever. After bearing the brunt of decreased recreational spending in 2020, the industry is riding the wave of ecommerce growth to top an unprecedented $500 billion in online credit card usage. Resurgent travel spending, higher wages and generous rewards programs all bode well for credit card payments.

But as card spending stabilizes among consumers, their issuers must contend with the broader impact of economic downturn.

Credit Card Payments Under Pressure

The country is seeing record numbers of credit card debt and growing delinquency rates. Economists at the Federal Reserve Bank of New York report that credit cards are the most prevalent form of household debt and expect this trend to continue—particularly with student loan payments resuming.

Talk of congressional action to lower swipe fees and rumors swirling around rising interchange fees also loom large for merchants that rely on credit card payments. With so much uncertainty, how can businesses protect their bottom line?

Bolster Your Business Growth With More Ways to Pay

Prepare for volatility in the credit card space by diversifying your payment methods. Consider these alternatives to safeguard your cash flow and generate revenue in any economic conditions.

4 Alternative Payment Methods

1. ACH

Automated clearing house (ACH) payments are a strong solution for businesses seeking reliability. This payment method allows merchants to draw funds directly from the customer’s bank account, limiting risk and excess costs.

ACH processing expenses are generally low compared to other forms of payment. Unlike credit cards, which are subject to fluctuating fees, ACH doesn’t require merchants to make authorization requests to credit card networks or issuing banks. This means that not only does using ACH save businesses money—it also insulates them from rising interchange fees if Visa or Mastercard choose to schedule increases.

ACH is also a more secure payment option. Credit card fraud is on the rise, with global losses projected to surpass $43 billion in the next five years. What does that mean for merchants? More chargebacks, less revenue and greater overall risk.

ACH payments also come equipped with security features that protect businesses from fraud. With end-to-end encryption and tokenization, sensitive payment data is disguised during transmission. It’s one of the safest payment methods available to businesses today.

2. Same-day ACH

Businesses can further optimize their electronic payments by implementing same-day ACH transfers. This method carries the same benefits as standard ACH payments, but with the added promise of receiving funds within a single day.

Payment processors traditionally could expect to see direct transfers reach their accounts in around four business days. But those that partner with a same-day ACH provider are guaranteed usable funds much sooner, provided they initiate the transaction by the designated cutoff time.

By bypassing processing delays, businesses enjoy the following advantages:

Faster payments, with lower fees. The speed of same-day ACH processing is comparable to credit cards. But with lower costs involved, the former provides merchants the best elements of both.

Streamlined cash flow. Automated transfers and reduced cycling times simplify delivery and allow for better control of cash flow.

Optimized customer experience. When you enable customers to pay their bills closer to the due date, both sides benefit. Same-day ACH processing helps last-minute payers avoid penalties, while faster crediting is applied to late payments.

Expedited payroll disbursement. Same-day ACH can also be used to pay employees via direct deposit. Faster issuance reduces administrative burdens by providing quick resolution of late payments or emergency distribution.

3. RTP

Real-time payments (RTP) can also quickly provide your business with cash flow. Much like ACH, this method supports quick electronic transfers between banks. But the similarities stop there.

RTP transactions are instantaneous—faster even than same-day ACH. These payments are initiated, cleared and settled with virtually zero perceptible delay. The unrivaled speed of RTP is a contributing factor to its international appeal: one 2020 survey found that consumers across six different markets consider real-time payments at least as important as internet access.

Speed isn’t RTP’s only convenient feature. Year-round availability is another unique benefit. Unlike ACH, real-time payments are also available on weekends, holidays and after business hours. Because it’s processed by The Clearing House rather than banks, RTP isn’t subject to the same limitations and enables 24/7/365 payments.

However, he RTP system isn’t always the answer. Transactions are capped at $1 million, and only credit payments are supported. Its network is also smaller than that of ACH—not every bank covers RTP.

But RTP is gaining popularity, and as it does, these drawbacks are expected to shrink. The U.S. Federal Reserve recently rolled out an instant payments service of its own in FedNow. As banks push for faster fund processing, the government’s network will offer them additional high-speed coverage options, making RTP more broadly available.

By stimulating competition with this move, expect to see increased adoption of real-time payments in the U.S.

4. Alternative Methods of Payment

Non-traditional payments are also available to businesses seeking credit card alternatives. To capitalize on these options, connect your bank account to an e-wallet that is compatible with popular payment methods. These might include:

PayPal

Physical or digital gift cards

Loyalty points

Apple Pay

Google Pay

Direct carrier billing

Offering customers the capability to use their preferred method encourages on-time payments, increased revenue and a seamless CX.

Get A Consult: Find Your Payments Fit

Payment methods should be built for your business—not the other way around. Connect with CSG Forte to get expert advice on which payment processing options will work best for you. Get started.

Mode of Payment – Guide to All Payment Types

Posted on

Cash, check or card—it wasn’t long ago that these were the only options people had when paying for a purchase. Today, customers have more choices than ever, including using their phones to pay at a store or restaurant or transferring money directly from their savings or checking accounts.

Accepting as many different methods of payment as possible allows your business to accommodate numerous customers. But first, you must understand what types of payments are available to use and what your company needs to do before accepting them.

What Is a Mode of Payment?

A mode of payment is how a customer pays for a purchase. When out with a group of friends, someone might pull out their phone and use a digital wallet to pay for a round of drinks. While shopping online, that same person may reach for their credit card to buy a new outfit. If they’re browsing a farmers market, they may hand over cash when purchasing their fruits and vegetables for the week.

The type of payment method a person uses can be dictated by what they’re buying and where they’re making their purchase. If they’re ordering online or over the phone, they can’t use cash or another physical payment form. Some merchants also prefer contactless forms of payment for in-person sales, as these are faster and easier than using cash or swiping cards.

Types of Payment Methods

Many payment methods are available today—integrating them into your operations is just a matter of which ones your business chooses to accept. Among your options are:

Card Payments

Card payments are convenient for customers, as individuals can carry less cash or make purchases online with their cards. Compared to cash, cards offer a sense of security. If a card gets lost or stolen, the cardholder can block it and report any fraudulent purchases made without paying for them.

Each type of card payment has different rules:

Debit: Debit cards typically connect to a checking or savings account. When a customer uses their debit card, the purchase amount gets pulled directly from their account.

Credit: Credit cards are a type of revolving credit or loan. When someone pays with a credit card, they are borrowing to make the purchase. Depending on when they pay their card balance, they may also have to pay interest.

Prepaid: Prepaid cards are similar to debit cards, but they don’t connect to a standard bank account. Instead, a person purchases a card for a specific amount, such as $200. Whenever they pay for something using the card, the purchase amount gets subtracted from the card’s balance.

Contactless: Contactless cards can be debit, prepaid or credit cards. Instead of inserting the card into a terminal or swiping it through a magnetic reader, a person paying with a contactless card waves or taps the card over an interface.

Phone Payments

Customers can use their phones to pay for purchases. They may place an order over a phone or use the device itself as a mode of payment.

Digital Wallets

Digital wallets store people’s payment card information on their smartphones. A customer can load their debit and credit cards to their digital wallet, along with gift cards for certain stores. Many digital wallets can communicate with credit card terminals through contactless near-field communication (NFC) technology.

Digital wallets are meant to be more secure compared to carrying around a physical card. To access the payment information, a person may need to input a special code or provide biometric information, such as their fingerprint.

People can use digital wallets when shopping online, too. When they use their digital wallet, they don’t share their credit or debit card number, making the transaction more secure.

IVR

Interactive voice response (IVR) is another payment method that uses a phone. Your customers can call into your messaging system and use IVR to pay a bill. The system is completely automated, allowing customers to access it 24 hours a day.

With customers paying over the phone, CSG Forte Engage enables leading organizations to streamline call center operations, improve payment security and enhance the customer experience. Businesses of all industries, ranging from government entities to insurance companies, can benefit from this user-friendly call center payment solution.

By Text

While people use their phones more than ever, they aren’t always making or receiving calls. Text messaging is often the preferred communication form. It can also be an easy way for customers to pay. Text to pay systems send customers a payment reminder through text. They can then click a link in the text, which directs them to a payment gateway.

Text to pay methods help ensure timely payments.

Online

Customers have many payment options when paying online, from inputting their credit card information on a checkout page to using their digital wallet. They can also pay through the Automated Clearing House (ACH) or eChecks to pull funds directly from their checking accounts.

Depending on the platform your company uses, customers can save their preferred payment method and information. The next time they visit your online store to place an order, all they need to do is click on their saved information to complete their purchase.

Buy Now, Pay Later

Buy now, pay later programs allow customers to split up payments into equal installments. Instead of $100 upfront for a sweater, a customer who chooses a buy now, pay later program can make four $25 installment payments. They can pay the first $25 after one month and then pay $25 per month for three more months.

When someone opts to use a buy now, pay later program, the company providing this service pays the merchant the full cost of the purchase (such as $100 for the sweater). The customer then makes payments to the buy now, pay later servicer. Whether they pay interest depends on the terms of the agreement and if they can keep up with the payment schedule.

Crypto

Most payment methods use the currency of the country your business is based in, such as U.S. dollars for U.S.-based companies. If your company accepts cryptocurrency, it receives payments in a completely digital currency. Crypto payments are based on the blockchain and are meant to be more secure than other forms of payment.

Benefits of Accepting Different Payment Types

Between credit card payment methods, digital wallets, buy now, pay later schemes and old-fashioned payment methods like cash and checks, you may feel your head start to spin. While you might want to keep it simple and limit the number of payment methods you accept, sometimes more is better.

You can reach out to more customers by casting a wide net and accepting more methods of payment. Everyone has their preferred way to pay, whether it’s a credit card, digital wallet or third-party payment system like Paypal or Venmo. You don’t want to alienate customers or turn down a sale because you can’t accept their preferred payment.

Accepting multiple forms of payment also creates a more positive customer experience and helps your business stay competitive.

How to Choose the Right Payment Method for Your Business

While you do want to accept multiple payment options, this may not be possible with all forms of payment. Your business’s format might automatically rule out some payment types. For example, if you’re entirely online, you probably don’t want to accept cash or paper checks, as doing so would mean you’d have to wait for those payments to physically arrive. You may also not want to deal with the hassle of setting up a crypto wallet.

Similarly, if your average order size is on the small side, such as less than $25, offering buy now, pay later options may not make sense.

Beyond that, consider your business’s structure. If you operate on a subscription model, accepting digital and card payments can streamline the process, as customers can provide their payment information once. ACH payments may be another appropriate option for a subscription-based company.

What to Consider When Choosing a Payments Provider

Once you’ve settled on the types of payment methods to accept, you need to choose a payment provider that offers them. There are a few essential features to look for in a payment provider.

Price: Providers use various pricing structures, such as taking a percentage of each transaction or charging a flat fee. Look for a provider with an upfront, crystal-clear pricing structure so you know what you’re paying and why.

Security: Your customers are counting on you to protect their payment information. Look for a provider that puts security first.

Scalability: Ideally, the payments provider you choose will work with your business now and accommodate your needs as your company grows in the future.

Revenue: The payment methods you accept influence how quickly your company gets paid for products or services. The right payment provider can help you boost your revenue.

Integrations: Your business may already use certain platforms, and you may wish to continue using those platforms. Look for a payment provider that integrates with your current systems.

Reporting: The more data you have about transactions, the better able you are to make decisions for your business. Choose a payments provider that offers insights into and reports on your transactions.

How Can CSG Forte Help Your Business?

CSG Forte is your partner in payments. We can help you grow your business through our unified payments platform. Whether you choose to accept payments online, by phone, in person or all of the above, we can help you do so.

Our platform quickly integrates with your current systems, allows for multichannel payments, and support is available when you need it. Our platform also has built-in Payment Card Industry (PCI) compliance and follows the industry’s highest security standards.

Choose CSG Forte

Expand your accepted payment methods and grow your business. Talk to us today to learn more about how we can help.

Everything You Need to Know About NFC Mobile Payments

Posted on

When customers use their phones to pay for purchases at supermarkets, restaurants or stores, those payments are in part powered by near-field communication (NFC). NFC is a type of wireless connection that lets two devices in close proximity to each other communicate. For instance, a smartphone with NFC enabled can send data to a nearby credit card terminal.

NFC makes paying more convenient for customers and businesses. If your company isn’t yet accepting NFC mobile payments, learn more about how it works and the benefits of using it.

What Is an NFC Mobile Payment?

NFC mobile payments are contactless payments. To make a mobile payment, a person must first have a smartphone with NFC enabled. They also need to install a digital wallet app on their phone. A few different digital wallets are available, including Google Pay and Apple Pay. Each type works with a specific type of mobile device. Apple Pay works with iOS devices, while Google Pay works on either Android or iOS devices.

Once someone has a digital wallet on their phone, they can load their payment information onto it. They will provide their credit card information, including their account number, expiration date and security code. The app stores that information securely. When they want to make a payment, they can open the app, choose their payment method and wave their phone near the credit card terminal.

How Does an NFC Mobile Payment Work?

NFC is a type of radio frequency identification (RFID) that lets devices communicate when they are within a certain range of each other while NFC is enabled. Most smartphones let users toggle NFC on and off. RFID isn’t new—it’s been used for decades in barcode scanners. However, NFC is a newer form of RFID—it’s been in use just since the start of the 21st century.

NFC uses a specific frequency that lets devices talk to each other when they are very close together. For an NFC payment to work, the user typically needs to place their mobile device about two inches away from the NFC-enabled terminal.

When an NFC-enabled mobile device with a digital wallet app installed gets within range of an NFC-enabled credit card terminal, the two devices start talking. When a customer opens their wallet, the NFC device will prompt a form of authentication, such as facial recognition, a fingerprint scan or a personal code. After confirming the user’s identity, the NFC device and terminal will establish a secure connection.

The smartphone sends encrypted payment data to the terminal, which then sends that data to the appropriate banks. The banks approve or deny the transaction, the data gets sent back to the terminal and mobile device, and the payment is completed (or declined).

The entire process takes just a few seconds. It’s usually much faster than swiping or inserting a credit card for payment and quicker than handing over cash and waiting for change.

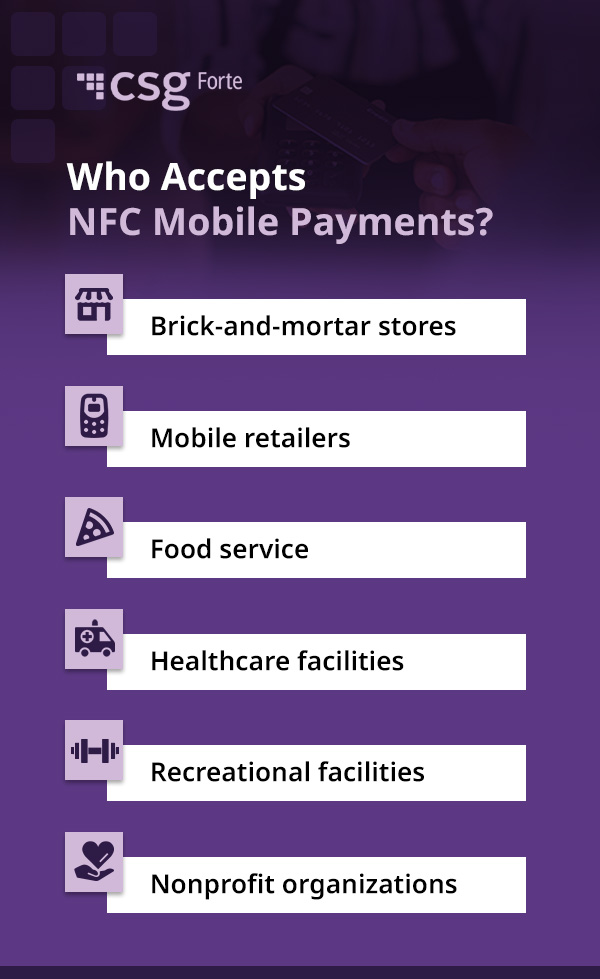

Who Accepts NFC Mobile Payments?

Many kinds of businesses use NFC payments. Although this method is rarely the only option a business offers, adding it to the list has many benefits. Businesses that process many payments in one day can especially benefit from NFC. This includes businesses like:

Brick-and-mortar stores: Antique dealers, clothing stores, home goods stores and similar locations offer NFC mobile payments.

Mobile retailers: Street vendors, flea market booths and similar traveling retailers can increase convenience with NFC payments.

Food service: Dine-in and carry-out restaurants offer NFC payments for contactless payment at the table or during pickup.

Healthcare facilities: Contactless NFC payments are common in pharmacies, hospitals, therapist offices, dental offices and other healthcare facilities.

Recreational facilities: Gyms, fitness centers and facilities serving individual customers can appreciate NFC payments.

Nonprofit organizations: NFC payments are an excellent way to enable convenient donations and fundraising.

Advantages of Using NFC Mobile Payments

NFC payments offer benefits to businesses and consumers. If you haven’t yet started accepting mobile payments, here are a few reasons to do so.

1. They’re Fast

A lot happens when a customer presents their mobile phone to pay, but it all happens nearly instantaneously. That’s because data travels from phone to terminal more quickly through NFC than it does when a card is physically swiped or inserted into the machine.

All that speed is good news for business owners, as it allows them to serve more customers in less time. It’s also good news for buyers, as they don’t have to wait a long time at the checkout counter for a sale to complete.

2. They’re Convenient

Who hasn’t forgotten their wallet at home, only to realize it when they’re at the front of the checkout line? With mobile payments, all a customer needs to do is pull out their smartphone to pay for their groceries, meals or new wardrobe.

NFC payments also allow for a smoother transaction process. Most people keep their phones within easy reach, but their wallets are securely tucked into a bag or pocket. Using mobile payment eliminates the need to dig around for a wallet. Customers also don’t have to wait for change or spend time counting out the correct number of bills.

3. They’re Secure

NFC mobile payments are as secure (if not more) than card payments—and they’re way more secure than using cash. If someone loses cash or has their wallet stolen, there’s no way to get it back. However, if someone loses their smartphone, they can lock it down to prevent anyone from accessing it or their payment information.

Digital wallets often have multiple security features built in to prevent unauthorized access. For example, a digital wallet may open up after the phone’s owner scans their fingerprint. Some apps use facial recognition software and only open after scanning the phone owner’s face. A slightly less secure option is for the app to require a person to input a code or draw a pattern before getting access.

When sending data from the phone to the credit card terminal, digital wallets encrypt the information. If a third party intercepts the payment data, they’d have to spend a lot of time and effort cracking the code and deciphering the information.

Some digital wallet apps also use a security measure called tokenization. Once the user provides their payment card information to the app, the app creates a series of random numbers, which it then uses in place of the payment card. Outside of the NFC payment system, the random numbers are worthless. If a third party gets access to them, they wouldn’t be able to use them for anything.

4. They Give Customers More Options

For some customers, the more payment options they have, the better. Adding NFC mobile payments to your business’s point-of-sale (POS) system means your customers have another choice when it’s time to complete a transaction. They can feel confident running to the store with only their phones.

5. They’re Flexible

Most digital wallets allow customers to use them for in-person payments—such as when someone is picking up their morning coffee or grabbing groceries after work—as well as for online payments, such as placing a weekly Amazon order.

6. They’re Easy to Set Up

Your business needs a terminal that accepts NFC payments before you can start accommodating digital wallets and mobile payments. If you use a complete payment solution, your card terminal will already be NFC-enabled, making it easy to start accepting digital wallets.

Once you have an NFC-enabled terminal, your business is ready to accept mobile payments from customers, speeding up their time in the checkout line and making life more convenient for everyone involved.

The Difference Between NFC and EMV

Europay, MasterCard and Visa (EMV) payments often appear alongside NFC payments in discussions, as they are both authenticated payments. While both methods offer convenient, secure and authorized payment methods, these methods use different technologies. EMV payments reflect the move away from magnetic strips and toward chip card payments. In many cases, swapping existing terminals to embrace modern models will allow you to embrace both payment types, expanding your flexibility. There may be other crossovers as well. For example, users may complete NFC payments by placing their device near the “tap” terminal location that accepts EMV payments. Additionally, some EMV-chipped cards support NFC technology.

NFC Mobile Payments Examples

Digital wallets turn smartphones into payment methods. The type of digital wallet a person has installed on their device depends on the operating system. Here are some of the most readily available NFC payment digital wallets.

Apple Pay

Apple Pay works on iOS devices, such as the iPhone, and preinstallation means users don’t have to download the app on their own.

Apple Pay users can save their credit or debit card information to the app, plus membership cards and gift cards. Individuals in the United States have the option of using an Apple Card or Apple Cash, which is a digital prepaid card. Users can choose which payment method to use as their default payment.

When someone wants to use Apple Pay to complete a purchase, they need to open and unlock the app using FaceID or their password.

Samsung Pay

Samsung Pay is similar to Apple Pay but only works on Samsung devices. It works the same way Apple Pay does, letting individuals save their membership cards, gift cards and debit or credit card details. Users can also take advantage of a prepaid Samsung card when using Samsung Pay.

For security, the app only opens after scanning the user’s iris or fingerprint.

Google Pay

While Apple Pay only works with iOS and Samsung Pay only works with Samsung, Google Pay works on Android and iOS devices. It allows users to save payment information that they can then access to make payments from the Google Pay app or when using the Chrome browser.

To use Google Pay, a person needs to verify their identity. They can use their fingerprint or a personal identification number (PIN) or draw a special pattern.

Addressing Payment Security With NFC

Like any payment method, understanding security risks and how to overcome them is crucial for your business and customer peace of mind.

A unique risk for NFC payments is an “eavesdropping” attack. NFC payments typically occur within short distances. The eavesdropping strategy allows unauthorized devices to receive a customer’s NFC signal during their transaction. This process can capture the information the customer is transferring, including card information. While this method typically requires equipment and a specific distance range, attackers will likely find ways to make overcoming these barriers easier.

Skimming is another possible risk. This attack strategy involves creating a fraudulent payment terminal to modify the existing one. The fraudulent terminal can capture the information of all NFC users who interact with it, which attackers can use to conduct unauthorized transactions or clone cards.

It is crucial to implement effective security strategies to combat these risks. Regular security checks, monitoring transactions and incorporating physical security can decrease the likelihood of an NFC attack. Proper staff training and partnering with reliable terminal and software providers can enhance your security practices and boost peace of mind.

Embracing NFC Payments With CSG Forte

Are you ready to accept mobile payments at your brick-and-mortar location? CSG Forte’s payment solution can help. Our platform makes it easy for customers to pay using their chosen method, whether it’s their digital wallet, a physical card or cash.

If you’re ready to streamline payment at your business, contact CSG Forte today to learn more about our payment solutions.

Tips to Reduce Late Payments by Engaging Payers

Posted on

Late payments are on the rise, and they can weigh down your organization’s growth if they go unaddressed.

Organizations are well aware how late payments can disrupt cash flow. As they add up, they can limit the ability to make the investments needed for growth, from purchasing new equipment, to hiring talent, to ordering inventory. Then there’s the cost of collecting late payments: sending out notices, attempting to call customers, engaging collection agencies, and so on.

So what can organizations do to help customers pay on time? By keeping them engaged with these approaches.

Make the payment experience as easy as possible

Many late payments result from transaction abandonment, which is a usually fixable problem in the customer’s payment journey. Sometimes the abandonment is accidental: think of how easy it is to get distracted in the process of paying a bill online or over the phone if it requires multiple steps. Other transaction abandonment is deliberate: perhaps the customer became frustrated to learn that they can’t make their payment online, and they put off the task for later.

To reduce transaction abandonment—accidental or otherwise—it’s important to make the payment experience as simple as possible.

Accept multiple payment methods.

You want to ensure most of your customers can use the payment method they most prefer, whether that’s credit/debit card, ACH, digital wallets, and yes, paper checks (55% of U.S. consumers wrote checks in 2022).

Offer auto-pay.

Automating regular payments is a win-win for you and your customers. Customers get to put the recurring payment out of mind, and your organization sees fewer late or declined payments. Offering and encouraging auto-pay makes a huge difference. Between April and July 2020, renters failed to make timely rent payments approximately 22% of the time. However, renters who used Rentec’s recurring payment system, powered by CSG Forte, only made late payments 1% of the time.

Allow payments in installments.

Making the payment experience easier can also involve offering a payment plan if your organization can provide that flexibility. Accepting partial or installment payments can be preferable to delinquent payments, and offering installments keeps the customer engaged. The key here is to use a payment solution that enables customers to set up their own alternative payment arrangements easily, without having to call into your call center. The payment terms, installment amounts and due dates also need to be clearly communicated to the customer through the user interface.

Send payment reminders on the customer’s preferred communication channels

The modern consumer has plenty of notifications and due dates competing for their attention. It’s easy for even your most organized customers to forget a payment unless they receive regular reminders. But reminders only matter if customers receive them on communication channels they use. Make sure you can send these automated messages by multiple methods, including email, text and outbound interactive voice response (IVR).

Also consider payment reminders that can integrate with customers’ calendar applications, increasing their visibility as part of your customer’s recurring to-dos. If you can enable seamless payments through your reminder communications, such as offering text to pay, then you’ve not only made it easier for customers to remember their bill, but also pay it in seconds.

CSG Forte Engage, a payer engagement platform, can help simplify your customers’ payment journey in these ways and more, enabling you to minimize late payments and protect your bottom line. Learn more about CSG Forte Engage and start increasing on-time payments today.

Taking Card Payments Over the Phone—Finding A Secure Approach

Posted on

Credit card fraud is widespread—and costly. A recent survey found that 65% of Americans with credit or debit cards have experienced credit card fraud at least once. Not surprisingly, 52% of U.S. bill payers rank security as a top feature in the digital bill payment process.

One area of heightened risk is taking credit card payments from your customers over the phone. Your organization needs to get paid and you can leverage tools to make taking phone and call center payments more secure.

Merchants who accept credit card payments must comply with the Payment Card Industry Data Security Standard (PCI DSS). Payment card brands may fine merchants up to $500,000 per incident if they aren’t PCI compliant at the time of a data breach.

Taking Credit Card Payments by Phone Is Risky Business

When consumers think of how contact center agents take payments, they often think of being asked to read off their credit card number, expiration date and CSV code over the phone.

If that doesn’t make you a little nervous—it should. That method of sharing card information may increase the risk of credit card fraud for several reasons:

A contact center agent may write the credit card information down on a piece of paper or somewhere visible where another person could walk by and steal the information.

A disgruntled employee taking the payment may steal the credit card information, using it to make unauthorized purchases or obtain funds from the account.

The customer may be in a public place when reciting credit card details. Someone may overhear the conversation and jot down the credit card information.

Reading out a CSV code negates the reason for having it—it’s used to prove the payer has possession of the card at the point of payment. Someone who overhears and captures that CSV can use it to make card-not-present charges.

2 Better, More Secure Ways to Take Credit Card Payments Over the Phone

Inbound and Outbound IVR — Customers pay via IVR (interactive voice response) with automated voice prompts and keypad inputs. This eliminates all three problems listed above. The contact center agent transfers the caller to the payment IVR system. The customer enters the card number, expiration date and CSV on their phone keypad when prompted to do so. The IVR system is integrated into a payment gateway to make the transaction. The system then gives the customer a receipt number and the option to receive the receipt by email. To make it even more convenient for your customer, you can leverage an outbound IVR, where a customer can schedule a time to receive an automated call to make their payment.

Live Agent Assist Technology — Businesses can leverage payments technology to have contact center agents quickly send customers a link to a custom online payment page for payment. By using a solution like CSG Forte’s Payer Engagement Platform, contact center agents can easily create an invoice with a few clicks of a mouse and send it to the customer via email or text message. This allows customers to pay promptly and securely—without sharing their credit card information with the agent. This method of payment greatly reduces the risk for fraud and the business’ PII data exposure.

The Payer Engagement Platform is a secure digital payment solution that enables customers to make payments using their preferred channel and payment method, at any time. Its Live Agent Assist feature allows call center agents to quickly create custom invoices to be sent to customers to complete transactions, eliminating the need for agents to collect sensitive information.

Why Does Your Business Need a Payment Service Provider?

Posted on

Payment service providers (PSPs) are pivotal in the digital payments landscape. Their services enable merchants of all sizes to accept various payment methods since consumer preferences differ. Retailers can gain more customers and increase sales by offering more payment choices.

What PSPs Do

A PSP is a third-party business partner that provides the technology required for merchants to take different payment methods from their customers. They help connect retailers to financial networks to support collecting credit and debit card payments, electronic bank transfers and more.

PSPs—also called merchant services providers—make payment collection simple, convenient, efficient and secure. They enable businesses to choose a processing option outside of their banks and generally work with numerous financial institutions and card networks. These broad industry connections help make the services more cost-effective and often come with additional features for more value. The result is a seamless payment experience for companies and their consumers.

Functions and services PSPs offer include:

Payment processing

Transaction security and fraud prevention