Reduce Late Constituent Payments With Automatic Reminders and Recurring Autopay

Key Takeaways

- Payment plans + recurring autopay can reduce government payment delinquencies without sacrificing fairness: Thoughtful payment plans paired with recurring payments help residents stay compliant while improving collections and reducing manual follow-up.

- Multichannel reminders work best when they’re timely and supportive: Email, text, and automated calls are most effective when sent before due dates and written in a clear, action-oriented tone.

- Unifying billing, payment channels, and revenue protection reduces workload: Bringing bill presentment, acceptance channels, and tools like account updater and NSF recovery into one platform cuts call volume and manual collections work.

When a resident falls behind on utility payments, a tax bill or a court fine, most government leaders see two bad options: send it to collections or write it off.

But often, the problem isn’t “won’t pay”—it’s “can’t pay all at once.”

Recurring government payments and structured partial-payment options give residents a realistic path to compliance while helping departments collect more of what they’re owed, sooner, and with less manual work. They also fit naturally into broader payment modernization efforts that move agencies off fragmented, legacy tools and onto unified, cloud-based platforms that support digital self-service across channels.

This article walks through why all-or-nothing payments backfire, where flexible options make the most sense, what to decide before rollout, how to communicate changes, and how to track impact on collections and staff workloads.

Why residents fall behind

Most delinquencies are about timing, friction, and confusion, not unwillingness. Common drivers include:

- Mismatched billing and pay cycles: Residents get paid weekly or biweekly, but bills are due on fixed dates that may fall just before payday.

- Bill shock and seasonality: Weather extremes, usage spikes, or rate changes can push even reliable payers into arrears for a month or two.

- High-friction payment experiences: If residents must mail a check, stand in line, or navigate a clunky portal, it’s easy to procrastinate. Internal guidance notes that outdated, single-channel portals often drive abandonment, unpaid bills, and more calls instead of self-service.

- Payment failures residents never see: Expired or reissued cards can silently break existing autopay arrangements, creating “mystery delinquencies” until a shutoff notice or large past-due balance appears.

At the same time, customer expectations have shifted toward digital, low-friction payments. Federal Reserve data from 2024 shows that nearly 70% of consumers prefer paying bills digitally instead of with checks or in-person payments, and more than half of U.S. consumers say they prefer mobile apps for government payments.

These preferences create an opportunity: make it easier to pay on time, instead of focusing only on penalties when payments are late.

Using reminders wisely (channel, timing, and tone)

Reminders are powerful, but if they’re poorly designed, they can feel intrusive. The goal is to send fewer, more relevant messages at the right time and on the right channel.

Channel: meet residents where they are

The right payer engagement platform should combine email, SMS, and automated calls to reach more diverse populations.

Consider:

- Email for full bill details, plan confirmations and receipts

- SMS/text for short nudges—“Your bill of $X is due on [date]. Pay now: [link]”

- Automated voice/IVR for residents who prefer or rely on phone payments

Timing: intervene before penalties and shutoffs

A typical cadence might include:

- Upcoming-due reminders 3–5 days before the due date

- Day-of nudges with a one-click or one-tap path to pay

- Early past-due notices (1–3 days after) that clearly explain options, including payment plans

- Installment reminders a few days before scheduled payments so residents can confirm funds

Tone: supportive and action-oriented

Especially in essential services, tone matters:

- Focus on information and options, not blame

- Clearly state amount, due date and what to do next

- When past due, highlight ways to avoid interruption—“Pay now,” “Schedule a payment,” or “Set up a payment plan”

This approach respects residents’ circumstances while still driving action.

Coordinating billing, customer service, and collections

Reducing late payments isn’t just a collections problem; it’s an end-to-end payments problem. Utilities see the best results when billing, customer service, and collections teams share one playbook.

Billing: clear presentment and unified channels

Billing teams can:

- Move more bill presentment online with EBPP (electronic bill presentment and payment) to send invoices electronically so customers can view bills and pay on their own, which speeds payment and reduces customer service calls.

- Consolidate payment channels into a single, integrated platform to reduce errors and confusion from fragmented systems.

- Ensure bills (paper and digital) clearly call out self-service options and how to enroll in autopay or payment plans.

Customer service: resolve issues and close the loop

Frontline agents need tools that let them help residents in a single interaction:

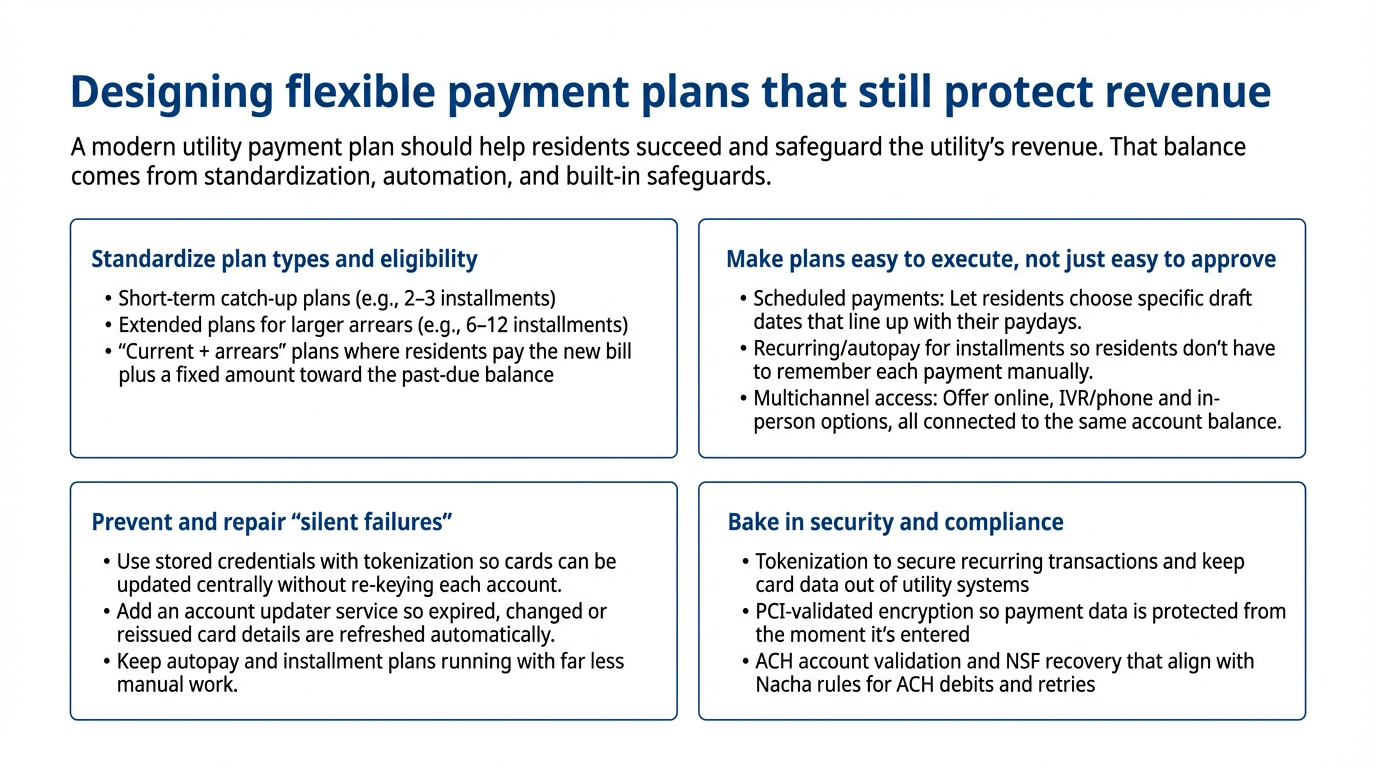

- Quick access to standardized plan options and eligibility rules

- The ability to send secure payment links during a call, so residents can complete payments on their device without reading card or bank details aloud (this also reduces PCI scope).

- Visibility into whether reminder emails, texts or calls were sent, to avoid confusing experiences for residents

Collections: focus on true non-payers

When plans, reminders and autopay are working, collections teams can:

- Spend more time on genuinely at-risk accounts instead of routine delinquencies

- Use analytics (e.g., frequent NSFs, chronic non-response) to prioritize outreach

- Work more closely with billing and CX to refine upstream policies and scripts

Real-world examples from adjacent sectors show what this looks like in practice. WasteWORKS, a solid waste management platform serving utilities and waste facilities, integrated CSG Forte to support online, in-person and card-on-file payments. Facilities now process payments “in seconds,” see fewer manual errors and have a seamless experience at every touchpoint, processing more than 144,000 payments each month through CSG Forte.

That same model—flexible channels with strong back-office integration—translates directly to utilities.

Bringing it all together with modern utility payment solutions

The most effective strategy doesn’t treat payment plans, reminders, and autopay as separate projects. Instead, it weaves them together into a single, modern payment experience:

- Clear, electronic bill presentment and self-service access

- Standardized, flexible utility payment plans tuned to resident realities

- Scheduled and recurring payments that align with pay cycles

- Automated, multichannel reminders with respectful language

- A secure, compliant infrastructure that protects both customer data and cash flow

CSG Forte’s utility billing and payment solutions are designed to support exactly this kind of approach, with omnichannel acceptance (online, IVR, in-person), payer engagement capabilities for reminders and flexible payment options, and secure electronic bill presentment.

If your organization is ready to reduce late payments, lower call volume and improve the resident experience, it may be time to revisit your payment strategy.

Talk with CSG Forte’s sales experts to explore how modern utility payment plans, reminders and recurring autopay can work within your existing systems and policies.

Frequently asked questions

- What is a utility payment plan?

A utility payment plan is an agreement that lets a customer pay down a past-due balance over time—often in fixed installments—while keeping current bills paid. Modern plans can be managed online, over the phone, or in person, and may support recurring or scheduled payments. - How do recurring autopay options reduce late utility payments?

When residents enroll in recurring payments for their monthly bill or plan installments, they no longer rely on remembering due dates. Combined with card updater and ACH validation tools, autopay can significantly reduce missed or declined payments. - What channels should utilities use for payment reminders?

Best practice is to combine email (for detail), SMS/text (for quick nudges and pay links) and automated phone/IVR for residents who prefer to call. CSG Forte’s payer engagement and utilities solutions highlight this multichannel approach to reduce delinquencies and support diverse customer preferences. - How can utilities keep flexible payment options secure and compliant?

Utilities should work with providers that support tokenization, PCI-validated encryption, ACH account validation, and Nacha-compliant NSF recovery. CSG Forte emphasizes these controls across its utilities and bill presentment solutions. - What metrics show that payment plans and reminders are working?

Track past-due rates by aging bucket, autopay, and plan adoption, card/ACH decline rates, billing-related call volume, and complaints about billing or shutoffs. CSG Forte customer success stories, like Hall’s Culligan and WasteWORKS, demonstrate how the right tools improve collections and reduce manual workload.