What Can ACH Processing With a Nacha-Preferred Partner Do for Your Business?

While digital payments have been around for decades, in the four short years since the pandemic made digital payments a bigger part of everyday life, Automated Clearing House (ACH) payment processing has become an integral part of digital commerce. The ACH Network—which is the only payment system that reaches all U.S. bank and credit union accounts—securely handled 31.5 billion payments valued at $80.1 trillion in 2023. In 2024, ACH payment volume increased 6.8% to $86.2 trillion—and its popularity is only expected to grow.

But as with any payment acceptance method, the stakes are incredibly high. Online shopping scams were the second-most common type of fraud reported to the Federal Trade Commission in 2023, which was the first year total reported fraud losses reported topped $10 billion. This heightened fraud risk and the financial damage that comes with it is why industry leaders lean heavily on payments partners preferred by Nacha, the nonprofit governing body behind the ACH Network.

So, let’s learn more about what ACH processing is, how ACH processing can impact your business, and why you should choose a Nacha-preferred payment partner to handle your company’s transactions.

What Is ACH?

ACH processing is a popular, reliable way to securely send and receive money—and you probably already use it more often than you know. For example, when your paycheck is deposited into your checking account, your employer is depositing your pay via ACH processing. If a customer makes a payment for your goods and services, the bank associated with your customer’s credit or debit card can deposit your funds directly to your business account using ACH processing.

ACH was designed to support increasing payment volumes as the world began to transition to automated payments. In the 1970s, financial transaction volumes were difficult to manage with early computer infrastructure. As a result, the Federal Reserve (i.e., the Fed) stepped in to fund an automated system of computer programs specifically designed to process and settle payment claims between financial institutions.

With ACH, merchants can process check and card payments without making authorization requests to credit card networks or issuing banks. Instead, ACH processing goes through the Fed or the ACH Network to secure payments from a receiving depository financial institution (RDFI). The RDFI then posts the payment into the requestor’s account.

This eliminates the need to pay network fees to a credit card company, meaning ACH payments cost much less to process. This saves merchants money with every transaction.

Nacha has repeatedly raised the daily transaction limit for ACH. This means that not only do ACH payments cost merchants less, but they can also accept much larger payments (up to $1 million per day) and recognize revenue faster.

ACH vs. Credit Cards: What’s the Difference?

No matter what payment options you offer, customers want to pay in the most convenient way for them. Often, this means they will use a credit card or another form of digital, contactless payments. But added convenience can also add costs. So what happens when a credit card payment is processed in the traditional way?

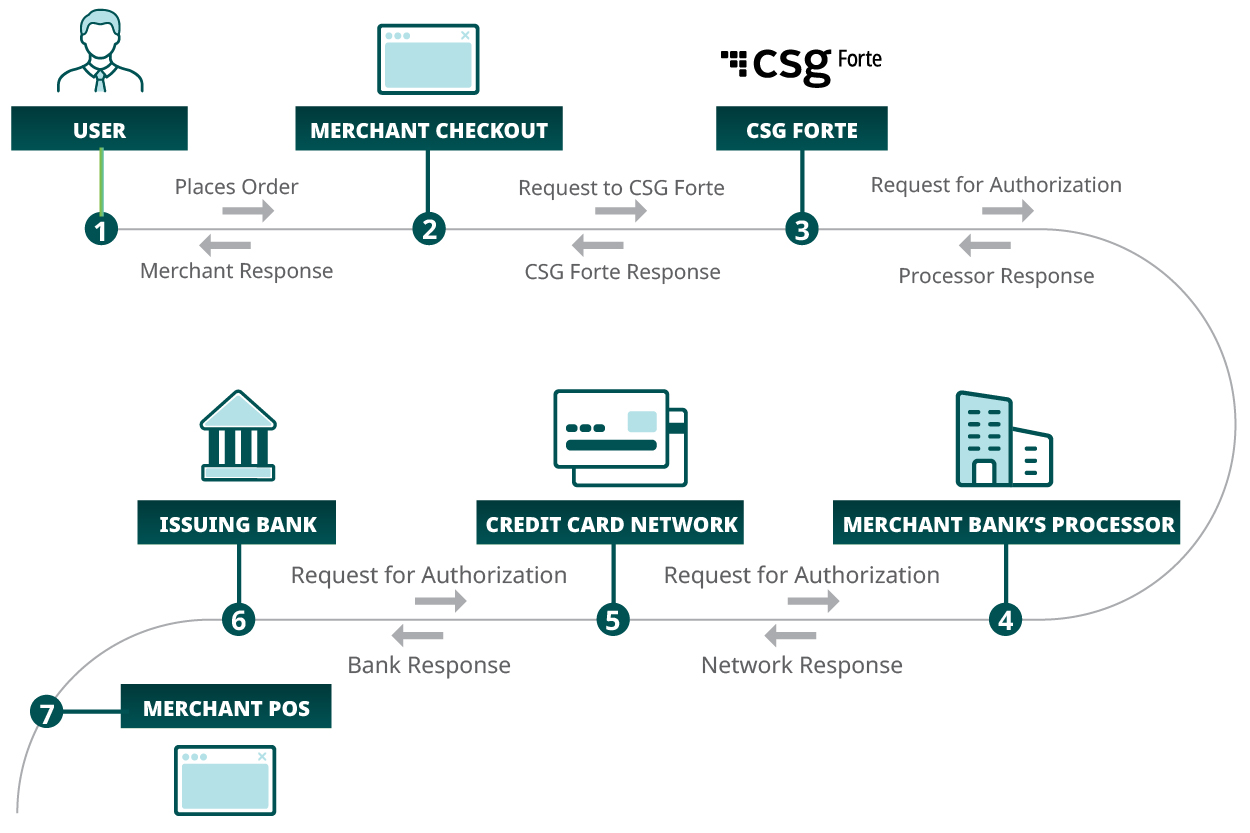

- The customer places an order or makes a purchase. The card information is received at point of sale.

- The merchant checkout accepts the card information and sends it to a service to manage the interactions with the merchant’s bank.

- The service sends the information securely to the merchant’s bank processor.

- The merchant’s bank processor contacts the credit card network, like Visa or Mastercard.

- The credit card network sends the request to the issuing bank for the customer’s credit card.

- The issuing bank determines if the purchase is authorized and returns that information to the credit card network who sends it back to the merchant’s bank process.

- The merchant’s bank sends to the merchant’s point of sale confirming if the payment is approved or declined.

Each of these steps adds cost. Each of these steps adds cost, as each entity involved in the transaction must get paid. Therefore, eliminating steps via adopting ACH processing reduces expense on top of adding efficiency.

ACH Processing

At first glance, the ACH payment process looks very similar, but there are a few core differences.

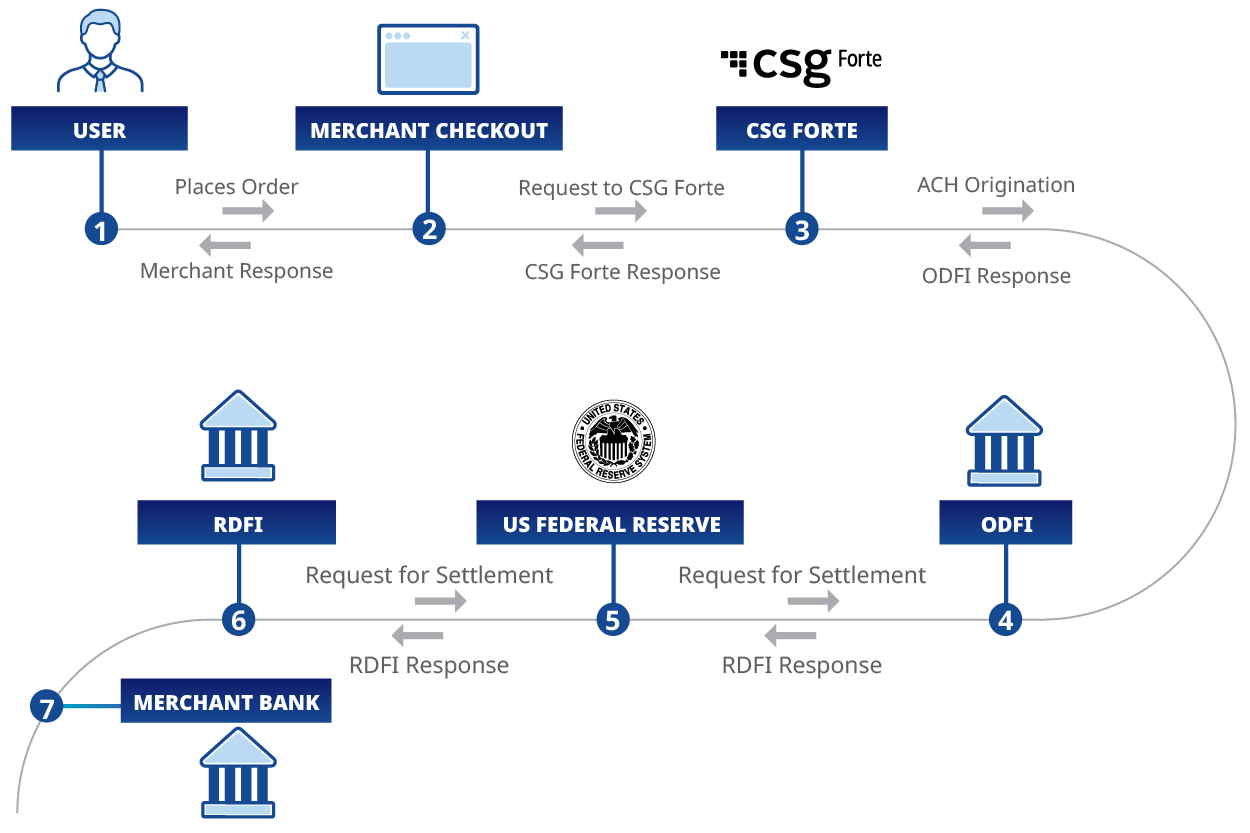

The ACH processing starts the same way at the point of sale before entering a processor’s system. But that’s where the similarities end.

- The customer makes a purchase. The account information is received at point of sale.

- The merchant checkout accepts the account information and sends it to a service to manage the ACH transaction.

- The ACH processor handles confirmation by contacting the originating depository financial institution (ODFI) for origination of the payment.

- The ACH payment request is sent through the ODFI, which requests settlement from the Fed.

- The Fed confirms that the payment is valid with the RDFI.

- The RDFI responds, by communicating back down the chain in reverse to approve or deny the payment.

- Funds are sent directly to the merchant’s bank account.

These last three steps are what make the difference in cost and security between ACH and traditional credit card payments. Because ACH avoids navigating several fee-incurring steps, the result is less costly and more reliable, especially when dealing with high transaction amounts as large as $1 million.

Standard vs. Same-Day ACH Processing

One major benefit of ACH processing is the speed a merchant can receive customer funds. For most ACH processors, funds may be available as soon as the next business day, depending on when the transaction occurred. Same Day ACH, which is newer, allows merchants to receive funds the same day the purchase was made.

Why does Same Day ACH processing matter? It’s simple: Same-day processing means merchants collect funds faster. This maximizes the benefit generated from ACH payments. Effectively, Same Day ACH lets merchants access payment funds quicker so they can invest in their businesses quicker. The increased cashflow from faster processing and fewer fees than processing credit card payments means that businesses who use Same Day ACH can get back to doing what they do best and worry less about transaction costs.

However, most payment processing companies do not offer Same Day ACH. And if they do, they do not own the technology. Merchants that work with payment processors that don’t own the technology are subject to additional fees for processing Same Day ACH.

CSG Forte is different. CSG Forte’s same-day ACH technology gives merchants the ability to receive funds quicker and more economically than they would by working with other payment processors.

3 Reasons You Should Only Choose Nacha-Preferred Payments Partners

Speed isn’t the only feature merchants should look for when shopping for a payments partner. Security and reliability are equally important. That’s why when considering payment processing options for your business, it’s crucial to understand the benefits of working with a Nacha-preferred partner. While there are many additional reasons (peace of mind at the top of the list), here are three of the most important reasons to stick with Nacha-preferred providers.

They validate everything: The payment processors that want to align with Nacha need to go through a strict validation procedure. Nacha also updates and develops more stringent rules and standards to offer the best possible security to its customers. That means you know the community of preferred partners on Nacha’s list follows the highest level of security standards. Stricter rules help with effective risk management and account validation services, thereby offering an additional layer of security against fraud.

They secure personal data: In addition to being innovators in transactions, Nacha-preferred partners also secure their customer data with best-in-class encryption. By signing up with these partners, you can feel confident that your account information and account numbers are locked behind a safe vault.

They partner with top financial institutions: Transferring money through ACH payment solutions is already significantly cheaper than moving it through credit/debit cards or wire transfers. Today, top technology providers are reducing the time to process ACH payments by partnering with financial institutions directly. By advancing the ACH network, Nacha has already reduced the time to process transactions over.

Your Business Needs ACH Processing

Simply put, ACH processing allows businesses to receive and have access to payment funds faster. Not only that, but the larger daily transaction limit means merchants can access more payments funds via ACH quicker, as well. Beyond the speed and convenience of ACH, businesses save money on each ACH transaction. Because they don’t need to pay settlement or interchange fees that arise from merchant networks, merchants can secure a larger chunk of each transaction. Especially when considering that compared to cash and paper checks ACH is also more secure and cannot be physically lost, it’s a powerful tool for businesses in many industries, from retail to healthcare and from financial services to real estate and telcos.

With the power that a great ACH solution can bring to your payments, it is no wonder that so many brands are adding it to their toolbox. However, if you’re interested in learning more about ACH processing or how you can get the most out of ACH with same-day processing, CSG Forte can help.

Ready to learn more about ACH and how it can drive more value for your business? Check out CSG Forte’s ACH processing capabilities.