Embedded Payments for Software Platforms: How ISVs Unlock Growth

For software platforms, payments used to be treated like plumbing—important, but separate from the product experience.

That no longer holds.

Today, the way your platform handles payments shapes how fast merchants get live, how easily end users complete transactions, how much operational friction your teams absorb, and how much revenue you leave on the table. For ISVs, embedded payments are no longer just a technical integration choice—they are a growth decision.

When payment capabilities live inside your platform, they stop being a bolt-on and start becoming part of the product itself. That shift can improve retention, reduce friction, and create new revenue streams—without forcing you to build a full payments stack from scratch.

Key takeaways

Embedded payments help software platforms reduce friction, strengthen retention, and create new revenue streams.

The difference between embedded and integrated payments is not just technical—it affects onboarding, support, control, and product stickiness.

Many ISVs can move faster by partnering with a provider instead of building a full payments stack from scratch.

What embedded payments mean for software platforms

Embedded payments are payment capabilities built directly into a software platform, so users can pay, get paid, onboard, and manage payment activity without being pushed into a separate third-party experience.

For software platforms, that means payments can become part of the workflows customers already use every day. Instead of redirecting merchants or payers to outside portals, your platform becomes the front door for the full payment journey.

That matters because software platforms do not win on payments alone. They win on experience. The easier it is for users to complete a task—from sign-up to settlement—the harder your platform is to replace.

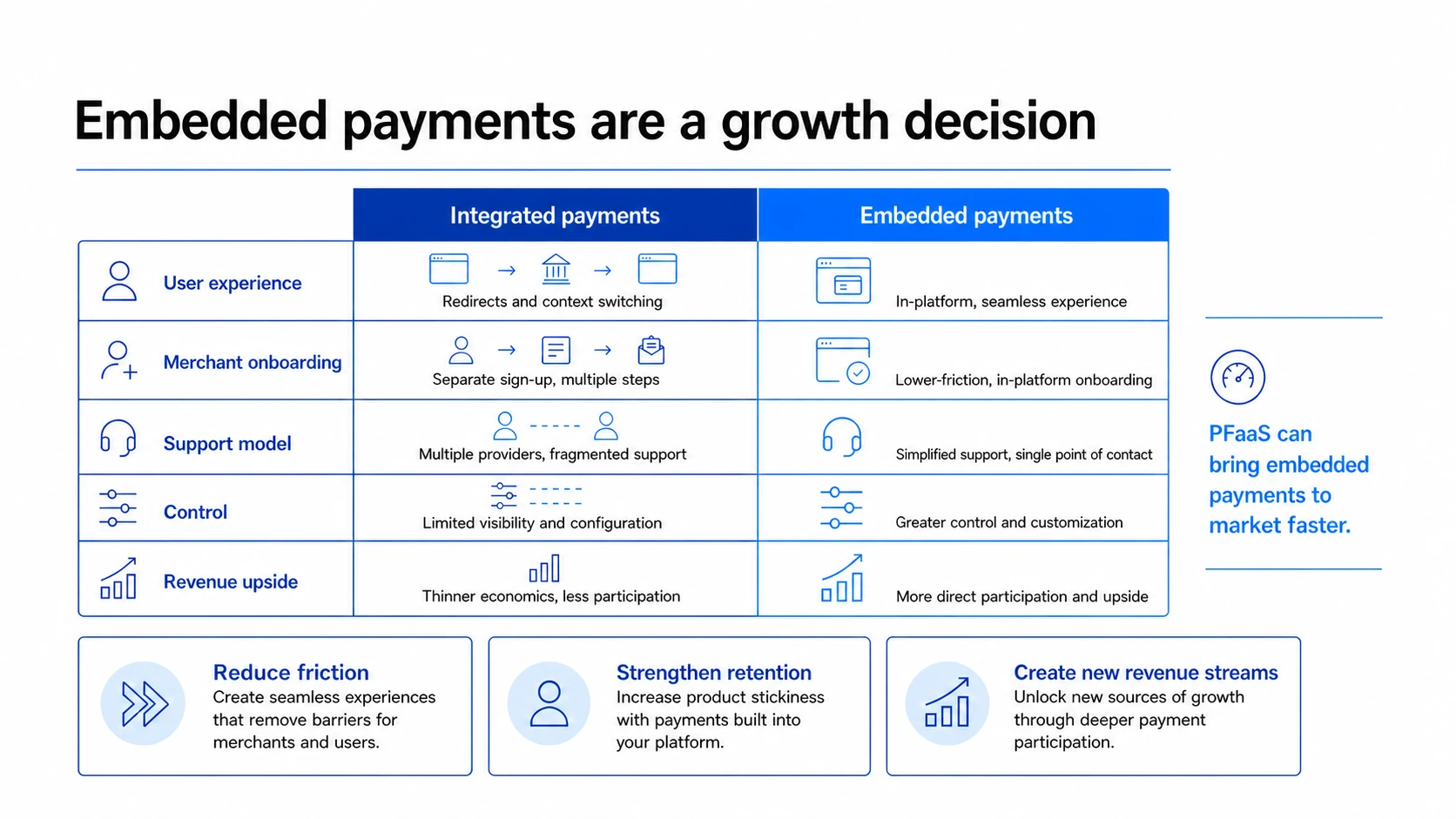

Embedded payments vs. integrated payments

The terms embedded payments and integrated payments are often used interchangeably, but they are not the same. If you want the broader definitional version, see what embedded payments are or the more operational breakdown in Embedded Payments, Minus the Hype: An Operators Guide.

Integrated payments usually mean the payment system connects to your software and exchanges data with it. That can improve accuracy and streamline some workflows. But the user may still encounter a separate module, a redirect, or a third-party environment that feels outside your brand.

Embedded payments take that a step further. The payment experience stays inside your platform. Onboarding, payment acceptance, reporting, and support feel like part of one system, not a patchwork of systems stitched together.

That difference has real business consequences.

With integrated payments, merchants often end up managing two separate relationships—one with the software provider and one with the processor. Support gets fragmented. Onboarding slows down. The payment experience feels generic. And because the processor owns more of the relationship, the software platform gives up both control and upside.

With embedded payments, the platform can create a more cohesive experience, simplify support, and build more durable product value around payments.

Why software platforms are embedding payments now

The biggest reason is simple: payment friction hurts growth.

When merchants have to leave your environment to apply, activate, or troubleshoot payments, they are more likely to stall, abandon the process, or blame your team for problems you do not fully control. That creates drag across onboarding, retention, and support.

Embedded payments help fix that in three ways.

They reduce friction for merchants and end users: Payments feel faster, simpler, and more trustworthy when they happen inside the platform the user already knows.

They increase stickiness: The deeper payments are woven into billing logic, reporting, onboarding, and everyday workflows, the harder it is for a customer to swap out your platform without disruption.

They create a stronger revenue model: Instead of settling for thin referral economics, software platforms can participate more directly in payment revenue and layer in value-added services that increase margin over time.

For many ISVs, that combination—better UX, stronger retention, and new revenue—turns payments from a back-office utility into a strategic lever.

What capabilities matter most

Not every embedded-payments program creates the same value. The ones that perform well usually share a few capabilities.

Fast, low-friction onboarding: If merchants cannot get live quickly, the rest of the payment experience does not matter. Strong embedded-payments programs make onboarding feel simple while still supporting the checks required for risk and compliance. For a deeper onboarding-focused companion piece, link to Merchant Onboarding for ISVs: Faster Flows, Stronger Risk and Compliance.

Flexible payment options: Software platforms need to support the payment methods their merchants and users actually want—whether that includes cards, ACH, recurring payments, text-to-pay, or other workflow-specific options.

Unified reporting and reconciliation: One of the biggest advantages of embedded payments is visibility. When payment and operational data live closer together, platforms can give merchants cleaner reporting and reduce manual reconciliation work.

Risk and fraud controls: Growth without control is expensive. Embedded payments should come with tooling for onboarding risk, fraud detection, account validation, and exception management—not just payment acceptance.

Branded, product-aligned UX: The best embedded-payment experiences do not feel like third-party add-ons. They feel native to the platform, consistent with the product, and clear at every step.

Build your own stack or partner?

This is where many software-platform teams get stuck.

At first glance, building your own payment stack can look attractive. More control. More customization. More upside.

But the real question is not whether building is possible. It is whether it makes sense for your stage, team, and risk appetite.

Building your own stack means taking on much more than checkout. You are now dealing with acquiring relationships, onboarding processes, risk controls, compliance responsibilities, settlement operations, support workflows, and the ongoing maintenance that keeps the whole system running.

That is why many software platforms take a partnership route instead—especially through payment facilitation-as-a-service, or PFaaS. If your team is actively weighing the path forward, Build or Partner? Embedded Payment Processing for ISVs is the closest internal deep dive on that decision.

A PFaaS model gives platforms a way to embed payments and shape the customer experience while offloading much of the heavy operational work behind the scenes. You keep more control over UX, monetization, and product strategy, while your partner helps handle the infrastructure, compliance, and risk layers that are costly to build alone.

For many ISVs, that is the practical middle ground. You get a faster path to market, a stronger revenue opportunity than a basic referral model, and less operational burden than becoming a full payment facilitator immediately. For a more partner-selection-focused lens, see How To Choose a Payments Partner for ISVs.

What to look for in an embedded-payments partner

If you are evaluating partners, focus less on generic “single API” promises and more on what will actually matter once the program is live.

Look for:

APIs and documentation your team can work with quickly

onboarding flows that help merchants go live without unnecessary delays

support for the payment methods and workflows your customers need

strong PCI, security, and compliance posture

fraud and risk controls that fit your operating model

modular capabilities, so you can expand over time instead of overcommitting on day one

responsive support for both your team and your merchants

The right partner should not just help you process payments. They should help you reduce friction, improve control, and scale the program as your platform grows.

Embedded payments are a product decision

For software platforms, embedded payments are not just about collecting money more efficiently.

They affect onboarding, retention, support, reporting, and monetization. They change how customers experience your platform—and how much of the payment value chain you actually control.

If your goal is to make your platform harder to replace, easier to scale, and better positioned to grow revenue, embedded payments deserve a more strategic role in your roadmap.

The strongest programs do not try to build everything at once. They start with the business model, choose the right operating approach, and partner where it creates leverage.

That is how software platforms turn payments into a growth engine—instead of another system to manage.

If you're ready to learn how PFaaS helps software platforms embed payments faster, reach out to one of our payments experts to schedule a call or demo.

FAQs

What are embedded payments for software platforms?

They are payment capabilities built directly into a software platform, so merchants and end users can complete payment-related tasks without leaving the platform experience.

How are embedded payments different from integrated payments?

Integrated payments connect payment functionality to software systems, but users may still encounter redirects or separate environments. Embedded payments keep the experience inside the platform’s own UI.

Do software platforms need to become payment facilitators?

No. Many platforms start with a partner or PFaaS model that allows them to embed payments and participate in the economics without taking on the full burden of becoming a registered payment facilitator immediately.

What should software platforms look for in a payments partner?

They should evaluate API quality, onboarding speed, compliance posture, payment-method flexibility, fraud controls, support quality, and the ability to scale with the platform over time.