Deposit Matching: How to Reconcile Non-ACH Healthcare Reimbursements Faster

Key Takeaways

- When reimbursements arrive as virtual cards instead of Automated Clearing House (ACH) payments, deposits and remittance data often travel separately, creating “mystery deposits” and slowing reconciliation for hospitals and physician groups.

- Straight Through Processing (STP) automates virtual card payments end to end, depositing funds directly into providers’ bank accounts and delivering matched remittance data for cleaner, faster deposit matching.

- Finance and revenue cycle leaders can pilot STP in 60–90 days, targeting high-volume, high-friction virtual card streams to reduce manual work, stabilize cash flow, and support growth initiatives.

Deposit matching should be the boring part of healthcare finance: cash hits the bank, remittance arrives, payments post, and the month closes on time.

But if a meaningful share of your reimbursements still come through virtual cards, payer portals, mailed notices, PDFs, or other non-ACH workflows, deposit matching becomes a daily scavenger hunt—because money and remittance don’t consistently travel together.

For many hospital finance teams and physician groups, deposit matching is where an otherwise “digital” reimbursement turns back into paper-era work. When payments don’t arrive via ACH—especially Optum and other payer virtual cards—your teams are left stitching together bank deposits, remittance files, and spreadsheets just to answer a basic question: What does this deposit belong to?

That last mile from “approved” to “deposited and reconciled” is slow, manual, and risky at exactly the moment margins, staffing, and growth expectations are under pressure. But it doesn’t have to be that way.

This article looks at why deposit matching is so hard when reimbursements aren’t ACH, and how Straight Through Processing (STP) from CSG Forte, in collaboration with Optum Financial, changes the equation for hospital administrators, physician group leaders, and CFOs.

What deposit matching is (and why it drives close speed)

Deposit matching is the process of linking a bank deposit to the underlying payment detail your teams need to post and reconcile cash—at minimum by payer and batch, and ideally down to claims/encounters.

When deposit matching works well, you get three outcomes:

- Faster posting (less “hold until we figure it out”)

- Cleaner reconciliation (fewer manual tie-outs and reclasses)

- Audit-ready traceability (an explainable path from deposit → payment detail → general ledger)

In modern reconciliation platforms, the goal is deposit-to-transaction traceability—being able to click a deposit and see the underlying activity for one-to-many reconciliation.

Why deposit matching breaks down without ACH

ACH tends to include consistent identifiers (trace numbers, addenda, standardized remittance), so your matching rules can be straightforward. But non-ACH reimbursement workflows often create the opposite conditions:

Payment and remittance arrive on different timelines

In many virtual card models, teams end up manually matching deposits to 835s, PDFs, or portal remits later. Even if both exist, they’re not reliably synchronized in a way your posting workflow can consume.

Key identifiers get lost in manual handoffs

When staff must retrieve card details, process payments like retail card transactions, and then re-key into billing systems, each handoff is a chance to drop the reference you need for clean matching.

Scale multiplies variation

Across multi-site organizations, local “shadow systems” (spreadsheets, notes, one-off rules) accumulate over time, which makes enterprise-wide matching and controls harder.

These problems are exactly what a modern payments solution streamlines for large hospitals and physician groups: quickly gets your accounts receivable ledger from “claim” to “cash” by replacing mail/portals and manual keying with an automated path where payment is processed automatically and deposited to your bank, and payment and remittance data are delivered together to support posting and reconciliation.

How Straight Through Processing supports faster deposit matching (when reimbursements aren’t ACH)

CSG Forte’s STP modernizes the “last mile” after a claim is approved—without changing payer adjudication:

- Optum sends virtual card + remittance data electronically to CSG Forte.

- CSG Forte processes the cards automatically—no manual keying.

- Funds deposit automatically into your bank account.

- Payment and remittance data are delivered together, supporting auto-posting where your systems are integrated.

Operationally, this is what deposit matching is supposed to feel like: fewer “What does this deposit belong to?” questions and less time keying and matching line items.

And because workflows matter as much as speed, STP is designed around governance and traceability—like the ability to trace each payment from Optum transaction ID → virtual card → bank deposit → general ledger.

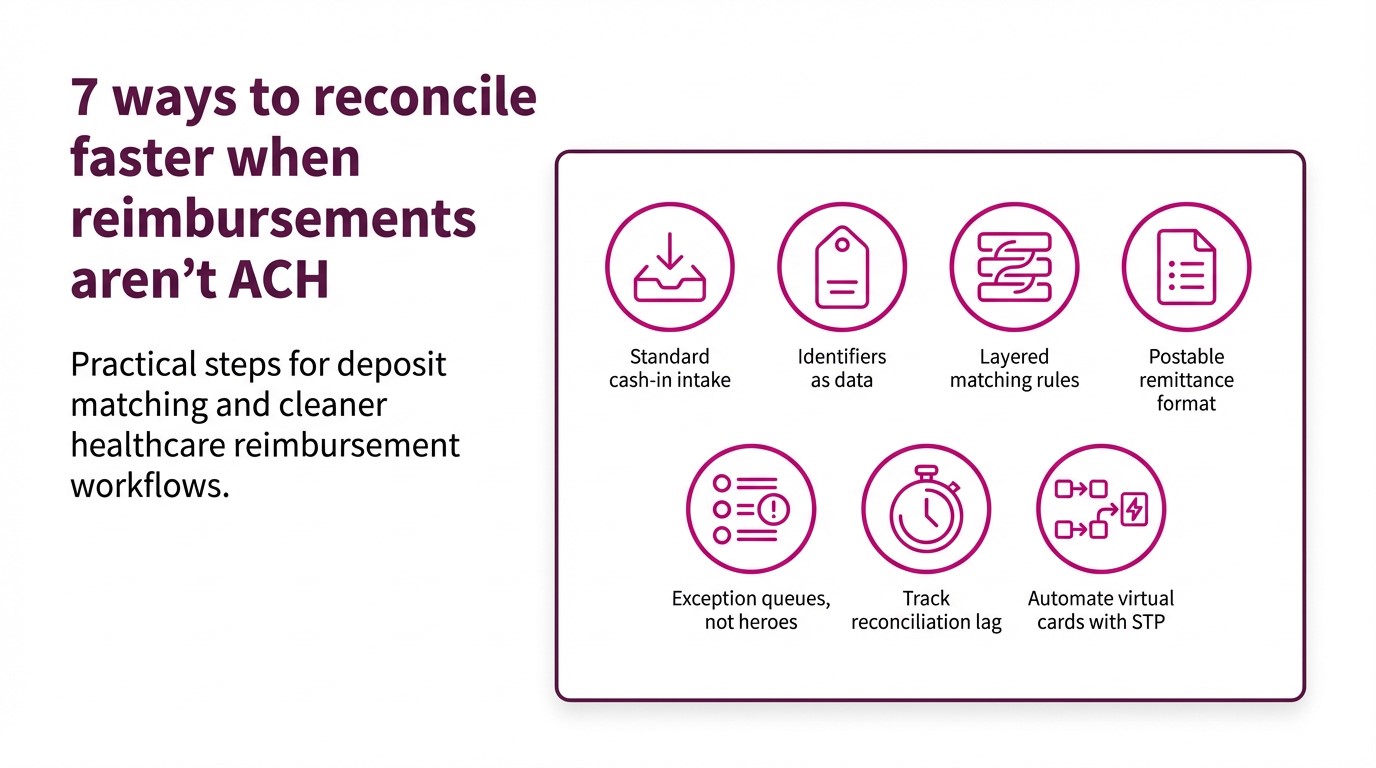

Next step: make deposit matching a system—not a hero exercise

If your team is still matching non-ACH reimbursements with spreadsheets and institutional memory, you don’t need more hustle—you need a tighter matching model:

- Standardize intake

- Preserve identifiers

- Automate the happy path

- Route true exceptions

- Shorten deposit-to-posted lag

Ready to reduce manual deposit matching for virtual card reimbursements? Sign up for CSG Forte Straight Through Processing to automate the last mile from “payment available” to deposited cash with aligned remittance data for posting and reconciliation.

Frequently Asked Questions

What is deposit matching in healthcare finance?

Deposit matching is the process of tying each bank deposit back to the underlying remittance advice—by payer, claim, patient and service line—so that payments can be posted accurately in your electronic health records system, practice management and general ledger systems. When it works, every dollar in the bank is transparently linked to what was billed, approved and adjusted. When it doesn’t, you see unapplied cash, manual research and reconciliation backlogs.

Why is deposit matching harder when reimbursements aren’t ACH?

ACH payments typically bundle funds and standardized 835 remittance data together, which many systems are designed to ingest and auto-post. With mailed or portal-based virtual cards, staff often run the card like a retail transaction and then manually search for the corresponding remit. Funds can hit the bank before remittance is available or properly mapped, creating “mystery deposits” and extra work to match and reconcile them.

How does straight-through processing improve deposit matching for virtual cards?

In the Optum + CSG Forte model, Optum sends virtual card credentials and remittance data electronically to CSG Forte instead of mailing card details. CSG Forte processes the virtual cards, deposits funds into the provider’s bank account and delivers aligned payment and remittance data through Dex and into connected revenue systems.

Does STP replace ACH EFT for hospital or physician group reimbursements?

No. STP is focused on automating virtual card reimbursements—including insurer payments and patient-via-payer payments—rather than replacing ACH. Many organizations choose to run ACH and STP side by side: they request ACH where it’s supported and use STP to handle the growing share of virtual card payments that won’t disappear in the near term.

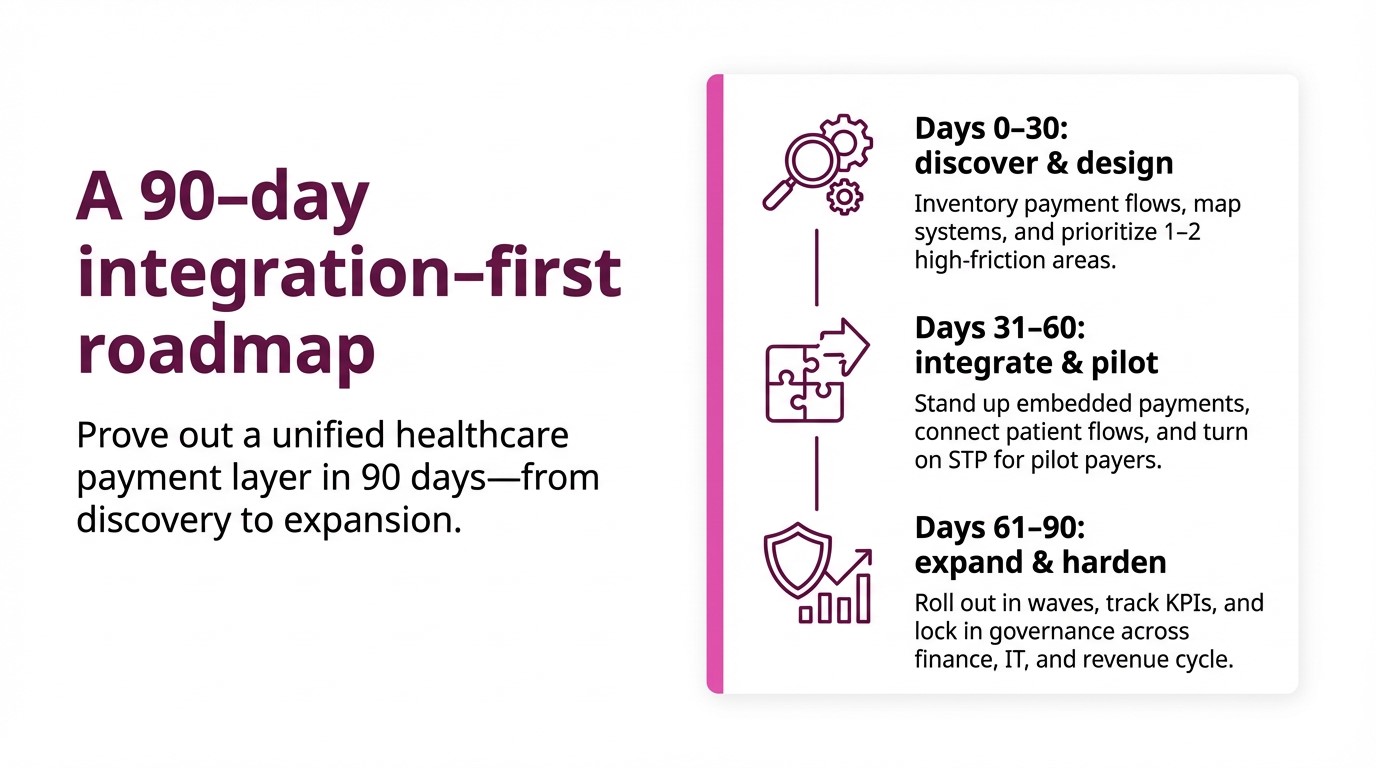

How quickly can we see reconciliation benefits from STP?

STP is a 90-day pilot-friendly initiative: 30 days to discover and map current virtual card flows, 30 days to configure enrollment and routing with Optum and CSG Forte, and 30 days to expand and tune based on early results. Because STP shifts virtual card streams from manual to automated processing, many providers see faster deposits, higher auto-posting rates and less unapplied cash within the first few cycles.