Loading...

Payment solutions for all businesses

Grow your revenue with payment solutions designed for the entire customer lifecycle.

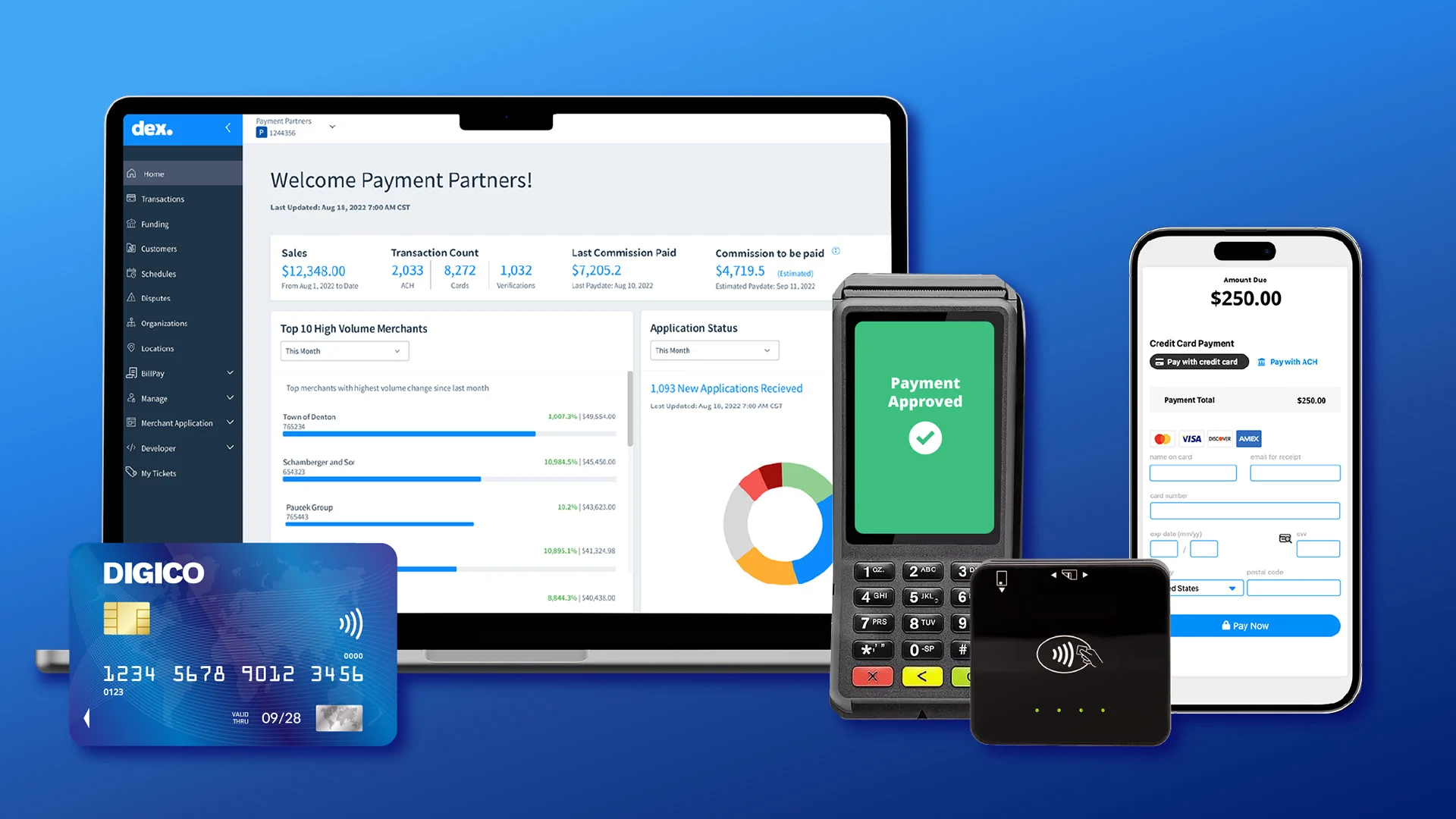

Unified Payments Platform

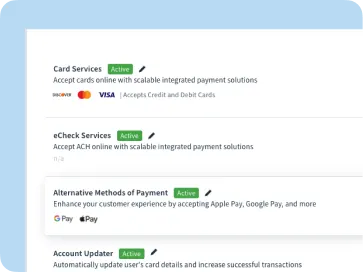

Allow your customers to pay how and where they want

Continue to evolve as your customer’s buying behaviors do by providing payment options that fit their lifestyles and grow your business (or revenues).

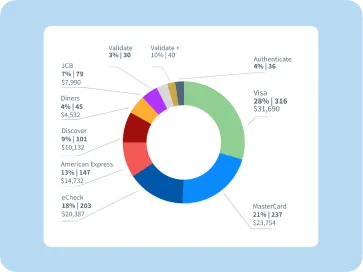

Enterprise-grade stability to manage billions of billing, payments and customer engagements each year

260M

transactions processed annually

25+

years of experience

Market fluency

Purpose-built for your industry

See why businesses rely on CSG Payments to power their full potential.

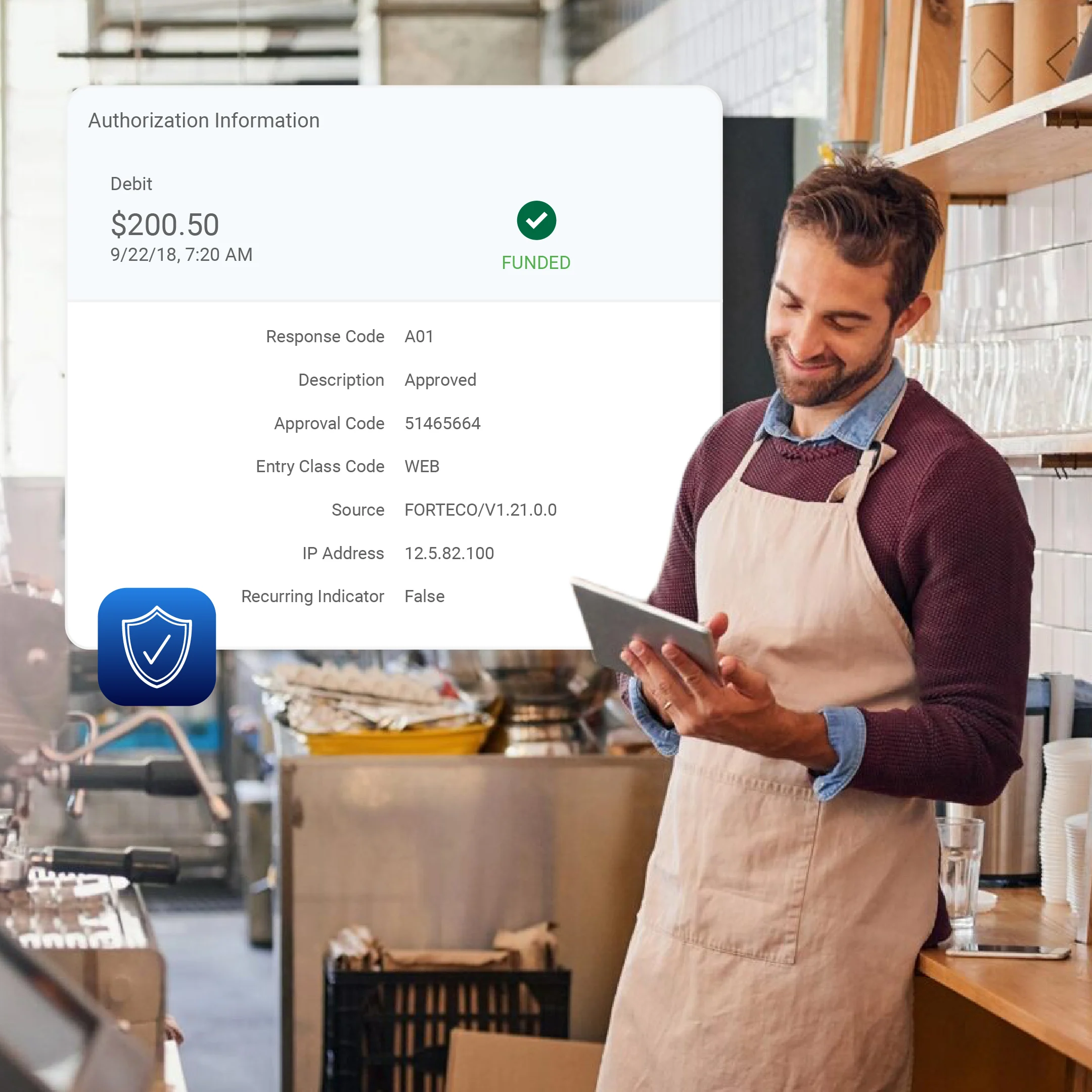

Focus on patient care, not payment paperwork

Streamline payment collections with HIPAA-compliant payment options. Whether you’re taking patient payments or closing insurance claims, we remove the manual work so your providers and facilities get paid faster.

Make payments your competitive advantage

Start taking payments almost immediately with our self-service onboarding. Give your customers the modern, fast experience they expect. Save money on every transaction with cost-effective ACH/eCheck processing, ideal for recurring billing models.

Customer Stories

Where market leaders go to grow

When industry leaders need to move billions of dollars without error, they rely on our infrastructure.

FOR > Home > Video

Expert analysis

Explore our latest thinking

Strategic insights and forward-looking trends to help you stay ahead of shifting customer expectations.

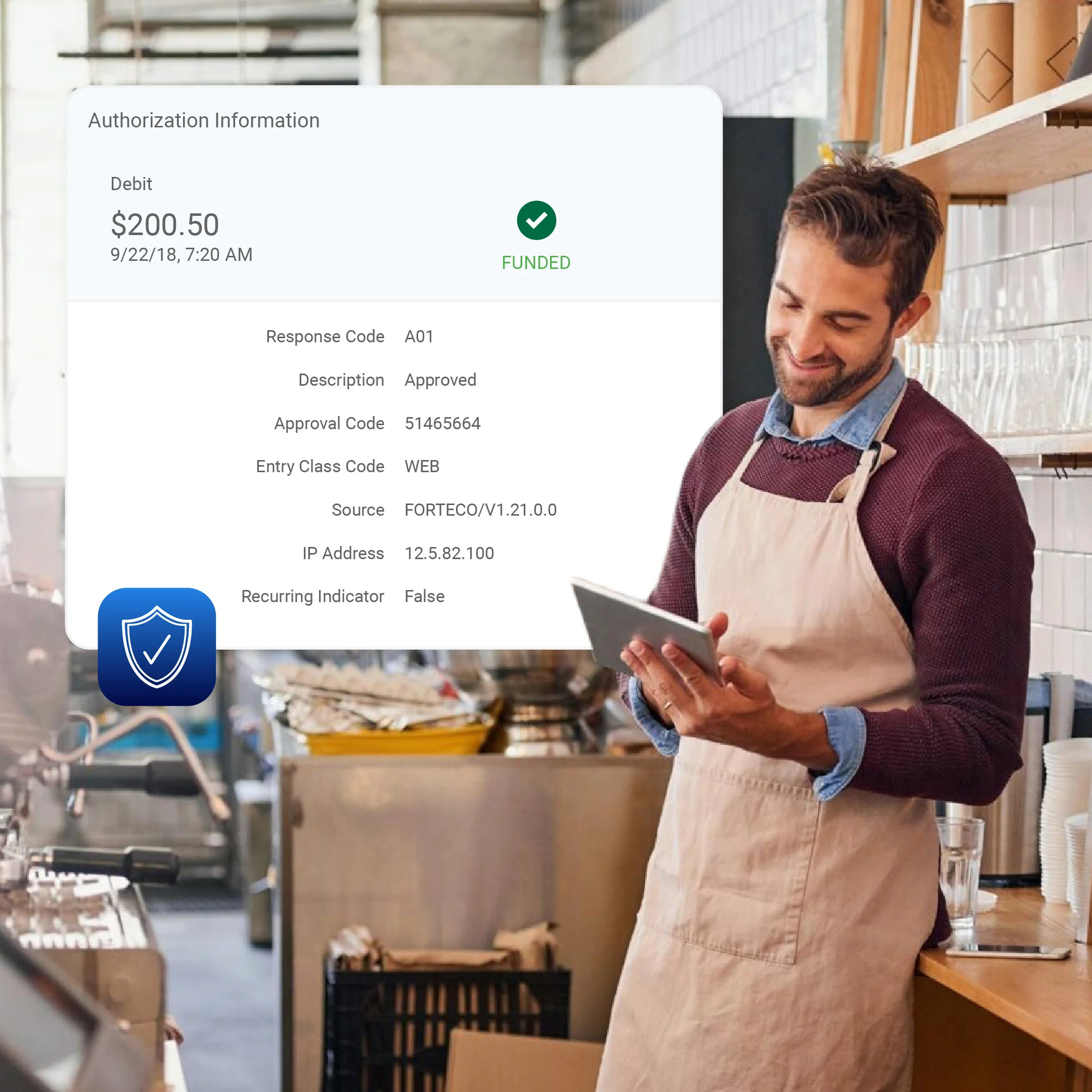

Security

Compliance that scales with your business

When you work with us, you’re working with a fully audited, secure, and compliant partner. From PCI to broader data privacy, we safeguard your payments and sensitive information wherever you're doing business.

Grow your payments revenue with a proven partner

See our platform in action or discuss your integration needs with a specialist.